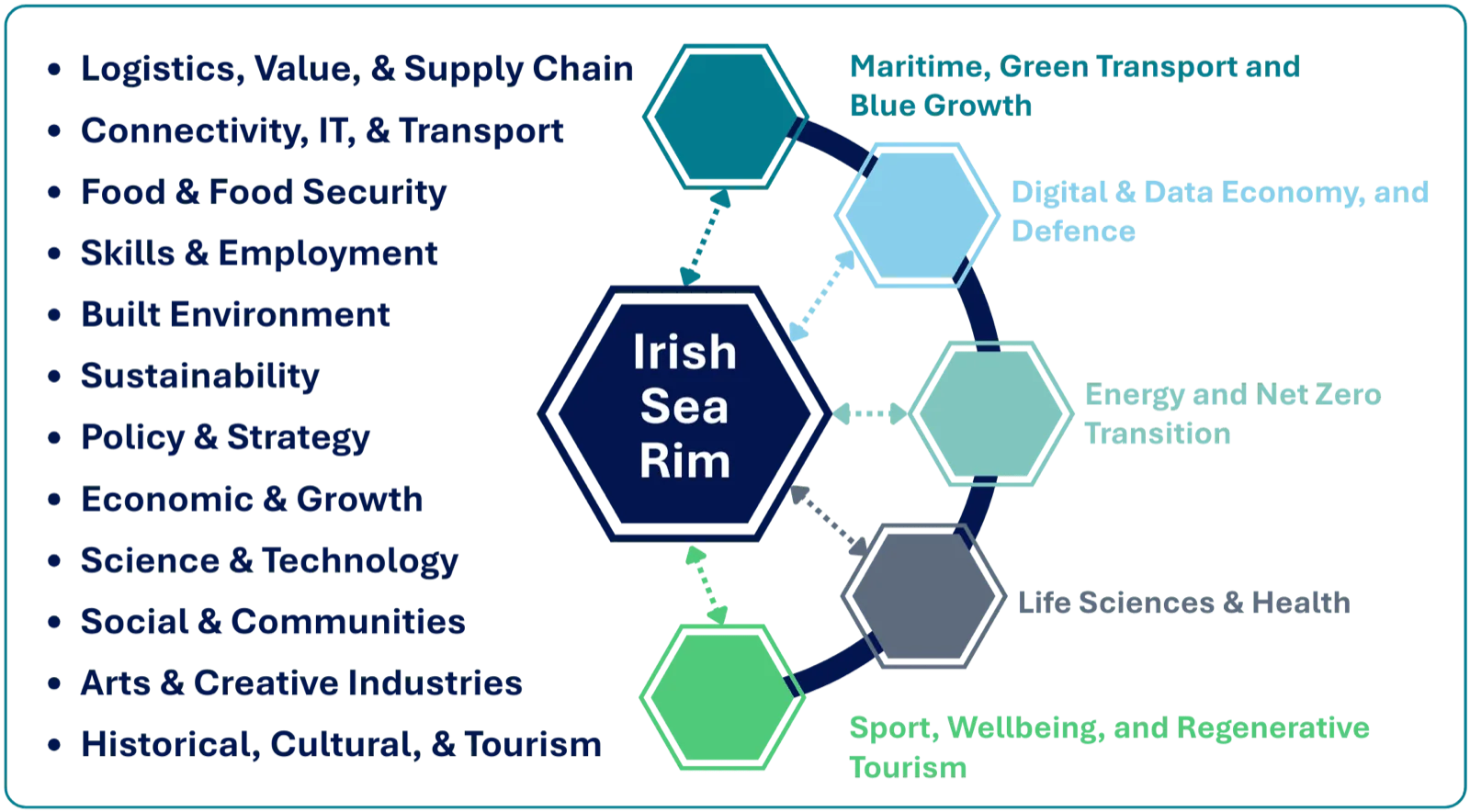

The Irish Sea is not just a body of water but a dynamic, interconnected economic and strategic arena, with critical sectors seeing significant investment, policy focus, and cross-border collaboration. Key sectors in which the Irish Sea Rim can help drive innovation and sustainable, inclusive economic growth are listed below and in Figure 6.1. Maritime is a central sector for the Irish Sea Rim and is examined in detail in Part Three of this report.

The Irish Sea Rim is an outward-facing, collaborative organisation designed to work across regions, sectors, and enterprises across the Irish Sea region, connecting and partnering with key stakeholders and enterprises including Tech Lancaster, Belfast Maritime Trust, Barclays Eagle Labs, Belfast Chamber of Commerce, Digital Isle of Man, LYVA Labs. Irish Sea Framework, Enterprise Ireland, Enterprising Cumbria, British Ireland Chamber of Commerce, MSPARC, OCO Global, North West Aerospace Alliance, and working with other collaborative bodies in the region such as the Irish Sea Maritime Forum and the Dublin-Belfast Economic Corridor. By connecting the collective knowledge of universities, institutions, businesses, and government agencies, the Irish Sea Rim aims to foster and support significant regional, national, and international projects and collaborations. The initiative will focus on several interconnected key sectors which define the region's economic and strategic importance (Figure 6.2).

ENERGY: POWERING THE FUTURE

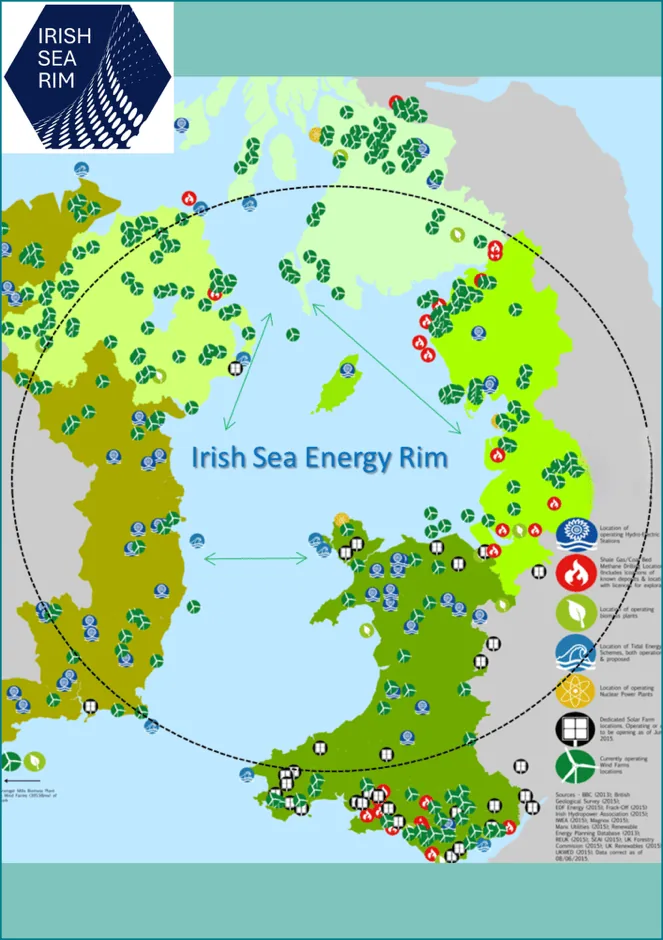

The Irish Sea is an undisputed energy powerhouse. As a focal point for energy production and with a long history of nuclear power on the coast of Britain, the Irish Sea is marked by a significant shift in investment towards renewable energy production.

The Irish Sea is an undisputed energy powerhouse. As a focal point for energy production and with a long history of nuclear power on the coast of Britain, the Irish Sea is marked by a significant shift in investment towards renewable energy production.

OFFSHORE WIND:

The region is a major hub for offshore wind development, with approximately 2.5 GW of operational capacity across multiple projects[4]. In July 2025, the UK government granted development consent for the Mona Offshore Wind Farm - a 1.5 GW project that officials described as "the largest offshore wind farm in the Irish Sea”[5]. With the completion of the Mona (1.5 GW), Morgan (1.5 GW) [6], and Awel y Môr (0.5 GW)[7] projects, the Irish Sea will host around 6 GW of capacity, making it one of the world's most concentrated offshore wind regions. On the right is a map of UK renewable energy locations around the Irish Sea.

Wind farm off Crosby Beach, north of Liverpool. Image credit: Irish Sea Rim

TIDAL ENERGY:

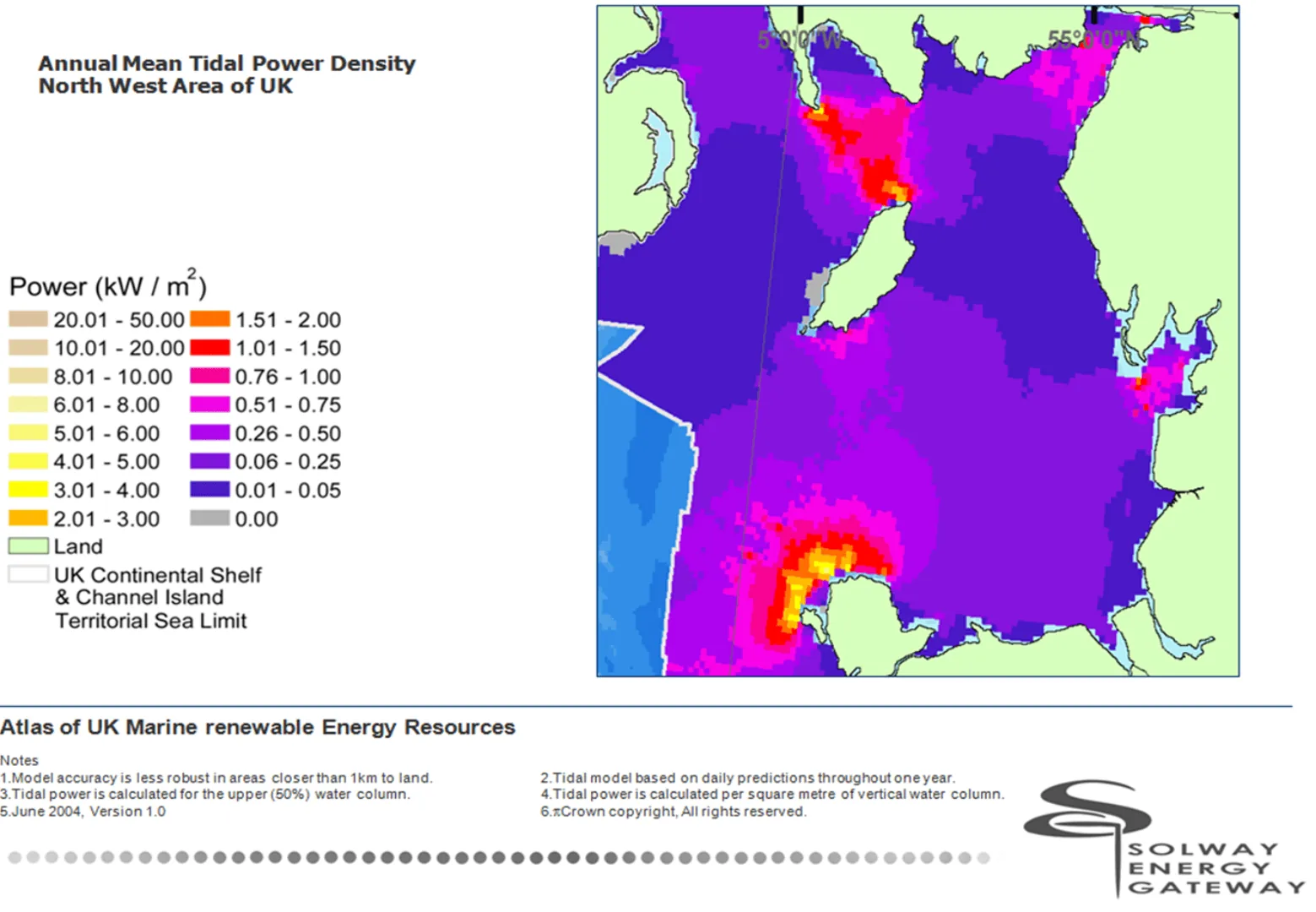

The Irish Sea is shaped by powerful tides and is emerging as a crucial hub for the United Kingdom and Ireland's ambitions in marine renewable energy (Figure 6.3). A significant and diverse portfolio of tidal energy projects, from world-leading demonstration sites to ambitious large-scale developments, are in progress at the advanced planning stage.

Current activity is focused on tidal stream technology, with one world-leading project nearing operation.

- MORLAIS MARINE ENERGY CENTRE, ANGLESEY, WALES: This is the most significant in-progress tidal project in the region. Morlais is a 35 km² consented seabed zone with a total potential generating capacity of 240 MW. Managed by social enterprise Menter Môn, its "plug-and-play" model provides the essential infrastructure – a large onshore substation connected to the National Grid and subsea export cables – for multiple technology developers to install and test their devices on a commercial scale. This de-risks development for companies deploying a range of floating and seabed-mounted turbines. First power generation is expected in the mid-2020s, marking a pivotal moment for the sector.

The future pipeline is dominated by ambitious, large-scale schemes that could transform the UK's energy map.

- MERSEY TIDAL POWER, LIVERPOOL BAY, ENGLAND: This is the most ambitious planned project in the Irish Sea. The proposal is for a large tidal barrage across the River Mersey estuary with a potential generating capacity of up to 700 MW – enough to power a million homes. Led by the Liverpool City Region Combined Authority, the project is in the advanced feasibility and consultation stage. If realised, its construction would be a major infrastructure undertaking, with a potential operational date in the 2030s.

- NORTHERN IRELAND PROJECTS: In line with the Northern Ireland Department for the Economy's Offshore Renewable Energy Action Plan, two major tidal stream projects are planned off the Antrim coast to harness the strong currents of the North Channel. The Fair Head and Torr Head projects each have a proposed capacity of around 100 MW. Although both projects have successfully secured seabed leases, they are now awaiting the final investment and consenting decisions that are needed to proceed to the construction phase. These developments represent a significant step towards achieving the region's marine renewable energy goals.

- OTHER REGIONS: Proposals for tidal energy projects in other areas, such as a barrage across the Solway Firth and developments off the Isle of Man, have been considered but have not progressed significantly in recent years.

PROJECT BRIDGE

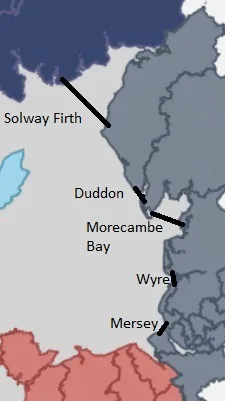

Project Bridge is a proposal to develop interconnecting tidal energy generating bridges across three major estuaries in Lancashire, Cumbria and Dumfries and Galloway. The potential tidal energy capacity available across the identified three sites, Morecambe Bay, Duddon Estuary and Solway Firth, is calculated to be in excess of 12GW. Apart from the overturning moments of the tidal flow the technology will create constant energy generation for an estimated 20 out of every 24 hours.

It is proposed to utilise a unique, cost effective, newly established, proven technology, which allows the existing tidal signal, within estuaries, to be maintained relatively unimpeded. This technology can be sited within the structure of a newly constructed bridge. Because it is not reliant on holding back the water flow, costly civil engineering work, associated with other methods of harnessing tidal power, are avoided. Also, due to the unique design of the technology, the environmental and ecological impact will be considerably reduced.

In additionally, a new and improved interlinking road could have a transformative effect in the region, resulting in highly significant positive social and economic benefits that open up many other development opportunities.

The proposal seeks to create a legacy project that is designed to benefit both present and future generations. In order to create benefit for the communities involved it is proposed that following investor payback, and reasonable period of return, a community wealth fund be established whereby the ongoing revenue stream is equally divided between the investors and the fund. The anticipated design life of the technology will be in excess of 120 years.

The proposal seeks to create a legacy project that is designed to benefit both present and future generations. In order to create benefit for the communities involved it is proposed that following investor payback, and reasonable period of return, a community wealth fund be established whereby the ongoing revenue stream is equally divided between the investors and the fund. The anticipated design life of the technology will be in excess of 120 years.

The BRIDGE project covers 3 of the illustrated tidal barrages in Figure 6.5. Morecambe Bay, Duddon and Solway Firth. Other projects in planning and consideration in North West England include the Mersey Barrage and the much smaller River Wyre scheme in Lancashire.

The West Coast of the UK has some of the highest tidal ranges in the world and this Irish Sea Rim coast is ideal to the development of tidal power infrastructure.

Figure 6.5: Proposed tidal barrages along the northwest England coast from north Wales to the Scottish Border

NUCLEAR POWER:

he Heysham 1 and 2 plants on the Lancashire coast provide a combined capacity of 2.4 GW[8]. On Cumbria’s coast, the Sellafield complex was formerly a reprocessing plant and now focuses on decommissioning.

ELECTRICITY INTERCONNECTORS:

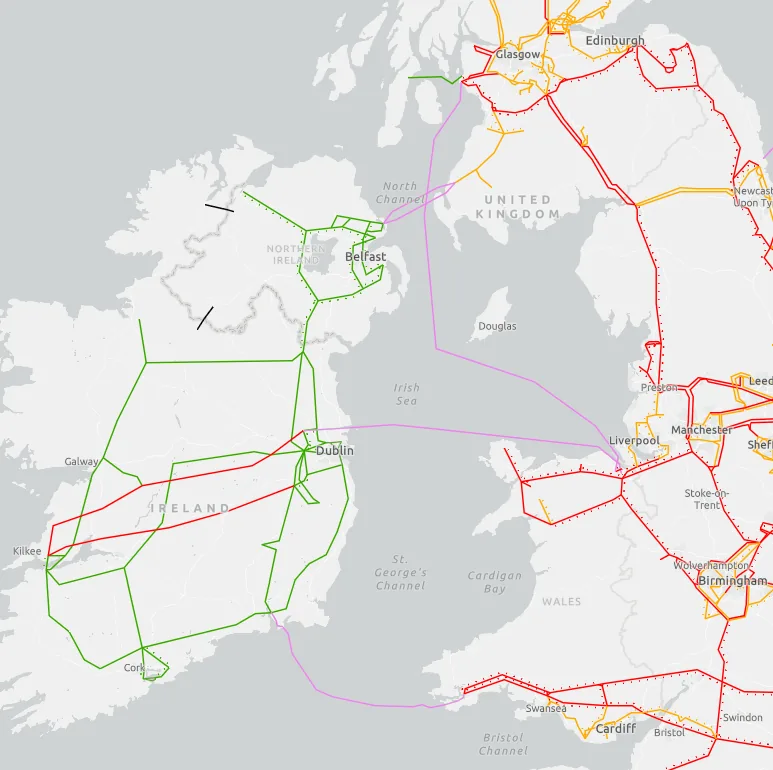

A robust network of subsea cables enhances energy security and trade (Figure 6.6).

Existing interconnectors:

Existing interconnectors:

- EAST-WEST INTERCONNECTOR (EWIC): 500 MW high-voltage direct current (HVDC) submarine cable linking Ireland and Great Britain[9].

- MOYLE INTERCONNECTOR: 500 MW HVDC submarine cable connecting Northern Ireland and Scotland[10].

- GREENLINK INTERCONNECTOR: Completed in 2025, this 504 MW HVDC submarine cable connects Ireland and Great Britain[11]. This interconnector doubles Ireland's interconnection capacity.

Figure 6.6: European Network of Transmission System Operators-E

Transmission System Map[12]

Planned / proposed projects

- CELTIC INTERCONNECTOR: A planned 700 MW HVDC submarine cable between Ireland and France, a joint project between EirGrid and RTE, now expected to be operational by spring 2028[13].

- MOYLE INTERCONNECTOR CAPACITY INCREASE: Plans exist to increase the capacity of the Moyle interconnector by directly connecting the converter station to a power station[14].

- MARES CONNECT: This proposed subsea cable between North Wales and Ireland would provide 750 MW of additional electricity capacity.

- LirIC: This proposed subsea electricity interconnector between Northern Ireland and Scotland may provide 700 MW of additional electricity capacity.

As Ireland’s grid faces increasing demands from the digital and other sectors, the existing interconnectors between Cumbria and Dublin, and the new interconnector between France and Cork are likely to come under increasing pressure. This may create the opportunity for exploring and researching the need for an additional interconnector between the UK and Ireland.

DATA CENTRES AND THE RISE OF AI

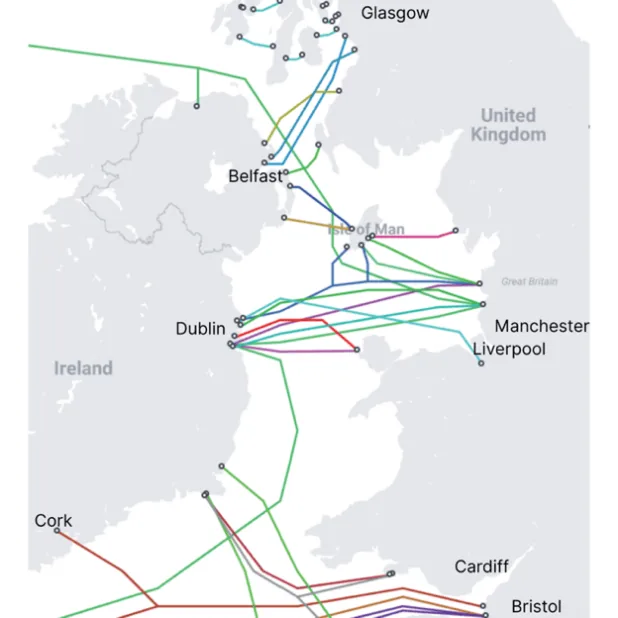

The region's role as a digital hub is accelerating, driven by connectivity, data centres, and a world-class semiconductor industry. The Irish Sea is a critical conduit for global data, hosting a dense network of subsea cables that form a primary asset, linking Ireland and the UK and providing vital transatlantic connections between Europe and North America (Figure 6.7). The Irish Sea coast hosts 36 data cable stations: Scotland (4), England (5), Wales (4), Northern Ireland (7), Ireland (10), and the Isle of Man (6).

The demand for data processing and storage, supercharged by the growth of AI, has led to a data centre construction and expansion around the Irish Sea. Dublin has joined Frankfurt, London, Amsterdam, and Paris as a top-tier European data centre market, and CWL1 in Cardiff, considered one of Europe’s largest data centre campuses[15], has been created to meet customer demand from around the world. A further nine data centres are planned in Wales, one in Scotland, five in Greater Manchester, as well as increasing numbers in London and the Greater South East of England.

The demand for data processing and storage, supercharged by the growth of AI, has led to a data centre construction and expansion around the Irish Sea. Dublin has joined Frankfurt, London, Amsterdam, and Paris as a top-tier European data centre market, and CWL1 in Cardiff, considered one of Europe’s largest data centre campuses[15], has been created to meet customer demand from around the world. A further nine data centres are planned in Wales, one in Scotland, five in Greater Manchester, as well as increasing numbers in London and the Greater South East of England.

Figure 6.7: Tele Geography Submarine Cable Map[16]

The UK data centre market is projected to reach £ 17 billion by 2030[17], with major data centres in Glasgow, Manchester, Liverpool, and Bristol, and the planned Atlantic Hub Data Centre Campus in Northern Ireland. The UK Government has classified data centres as critical national infrastructure, meaning that they will get extra support during major incidences such as cyber-attacks, connection disruptions, or extreme weather to minimise disruption.

Blackpool's Silicon Sands initiative is a key new development which will create a major tech hub with its campus of eco-friendly data centres[18]. Launched in 2024, it aims to create a carbon-friendly data campus powered by renewable energy. By combining its direct connection to the CeltixConnect-2 subsea internet cable - linking North America to Northern Europe – with liquid cooled and solar powered data centres, Blackpool will become a critical transatlantic data gateway.

It is critical to note that the explosion in AI is driving unprecedented energy demand in both the UK and Ireland. The UK has established an AI Energy Council bringing together energy providers, tech companies, energy regulator Ofgem and the National Energy System Operator (NESO) to forecast energy needs for a twenty-fold increase in compute capacity over the next 5 years[19]. A recent BBC News article cited concerns about environmental impacts and the knock-on effects on energy bills in regions with major data centres[20].

Ireland already faces acute pressure, with data centres consuming 22% of the country's electricity in 2024[21] and projected to reach nearly a third by 2026[22]. In February 2025, Ireland’s energy regulator the Commission for Regulation of Utilities (CRU) proposed policies requiring any new data centres connecting to the electricity network will be required to provide on-site or local generation and/or storage capacity to match the requested connection capacity[23].

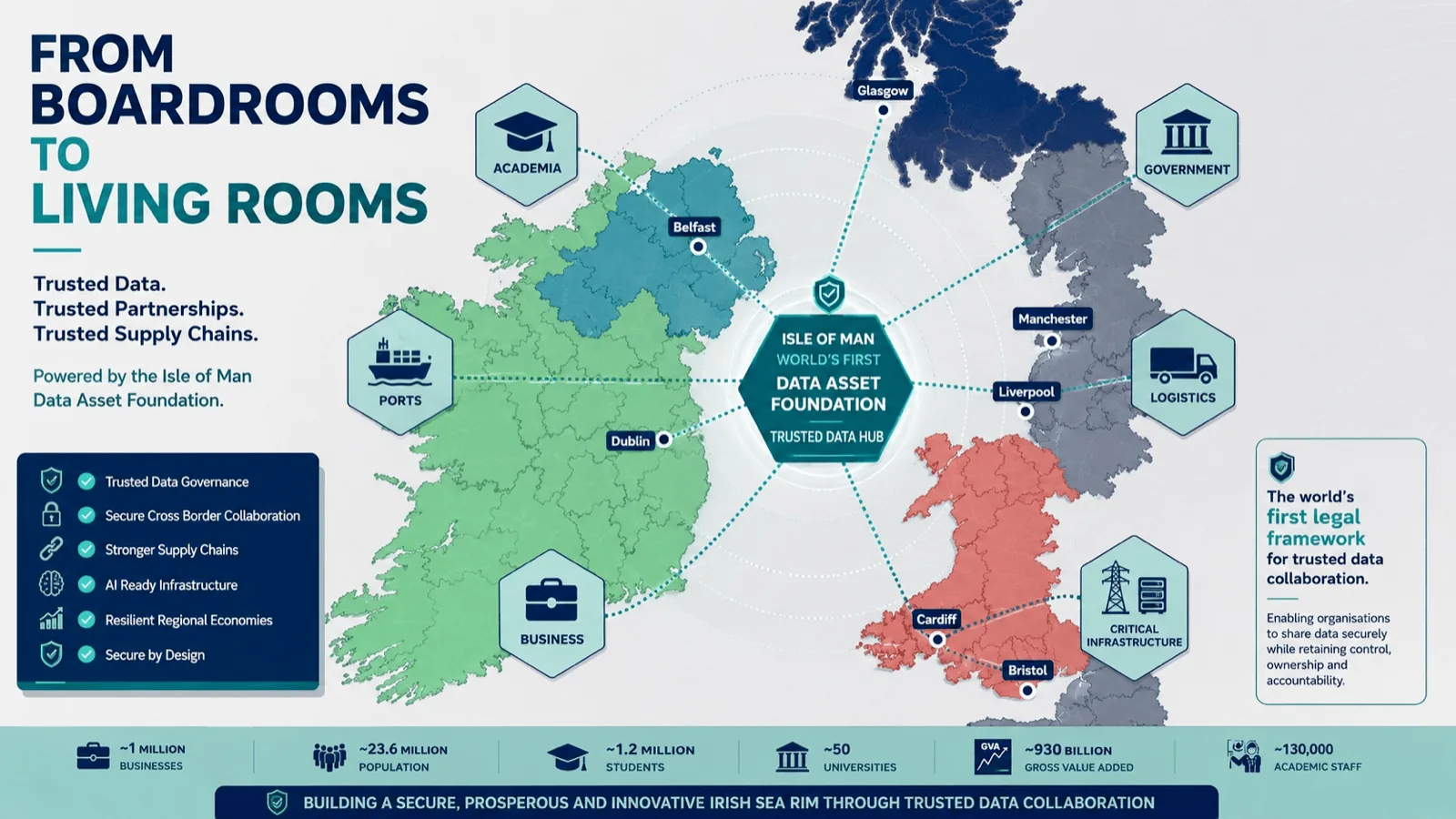

ISLE OF MAN DATA ASSET FOUNDATION

Within the digital and data economy, the Isle of Man has an opportunity to establish itself as the trusted data hub of the Irish Sea Rim. Through the world’s first Data Asset Foundation legislation, the Island can provide a governance framework that enables organisations, ports, universities, public bodies, and businesses to collaborate securely whilst retaining ownership, control, and accountability for their data. This capability directly supports the Irish Sea Rim’s ambitions around digital infrastructure, artificial intelligence, cybersecurity, innovation ecosystems, and cross border collaboration.

From a strategic perspective, the emergence of the Isle of Man’s Data Asset Foundation framework represents a significant shift in how organisations can govern, protect, value and utilise data. Historically, data has been treated as an operational byproduct despite becoming one of the most valuable assets in the modern economy. Data Asset Foundations provide a trusted legal and governance structure that enables data to be managed as a recognised asset, creating greater transparency, accountability, and long-term stewardship. This allows organisations, governments, research institutions, and industries to collaborate around shared data resources whilst maintaining appropriate ownership, control, security, and usage rights. In effect, a Data Asset Foundation creates the institutional infrastructure required to unlock the economic, social and strategic value of data in the same way that trusts, foundations and corporate structures unlocked the value of financial and physical assets.

The potential applications are extensive and span almost every sector of the economy. In the maritime sector, Data Asset Foundations could support the creation of trusted data ecosystems connecting ports, vessels, regulators, insurers, classification societies, logistics providers, and technology companies. This could enable the secure sharing of operational, safety, environmental and maintenance data to improve vessel performance, strengthen maritime safety, accelerate decarbonisation, and support the deployment of AI enabled services. Beyond maritime, Data Asset Foundations could underpin carbon accounting systems, healthcare data collaboration, digital identity frameworks, smart city infrastructure, supply chain resilience, scientific research, energy transition programmes, and regional economic development initiatives. By providing a neutral and trusted governance model, they offer a mechanism for organisations that would not traditionally share data to collaborate safely and confidently, creating entirely new forms of value, innovation, and economic opportunity.

Data Asset Foundations have the potential to become foundational infrastructure for the AI economy. Just as financial markets depend upon trusted institutions to govern capital, the next generation of AI systems, digital services and data driven decision making will require trusted institutions to govern data. Jurisdictions that establish these frameworks early have an opportunity to position themselves as global centres for trusted data stewardship, attracting investment, innovation, research activity, and high value industries. In this context, the Isle of Man’s leadership in establishing a legal framework for Data Asset Foundations positions it at the forefront of a rapidly emerging global market where trust, governance and data ownership are becoming as important as the data itself.

SEMICONDUCTORS

The Irish Sea region is a powerhouse in the global semiconductor industry. South Wales’s CSconnected is the world's first dedicated compound semiconductor cluster[24]. As of 2024, it reported employing nearly 2,750 people and contributing £366M in GVA[25]. It continues to attract significant investment, including a recent £51 million injection into the Newport Wafer Fab facility[26], while Glasgow’s planned National Advanced Semiconductor Packaging and Integration Centre will create a national hub for the development of advanced semiconductor packaging[27]. Northern Ireland has specialised in Silicon-on-Insulator (SOI) manufacturing capabilities[28].

Bristol anchors the "Silicon Gorge" tech cluster, ranked as UK's second-largest tech cluster with 10,000 tech companies[29]. The Liverpool-Manchester corridor serves as a critical R&D hub for the semiconductor industry, with activities and investments including the National Graphene Institute, the Science and Technologies Facilities Council (STFC) Daresbury Laboratory, and the Semiconductor Detector Centre.

Ireland has established itself as Europe's semiconductor manufacturing leader[30], with international players operating in Dublin and Cork. Its robust semiconductor industry is impressive: 130 companies, 20k jobs and € 13.5 billion in annual exports. The Silicon Island strategy aims to create up to 34,500 new semiconductor roles by 2040.

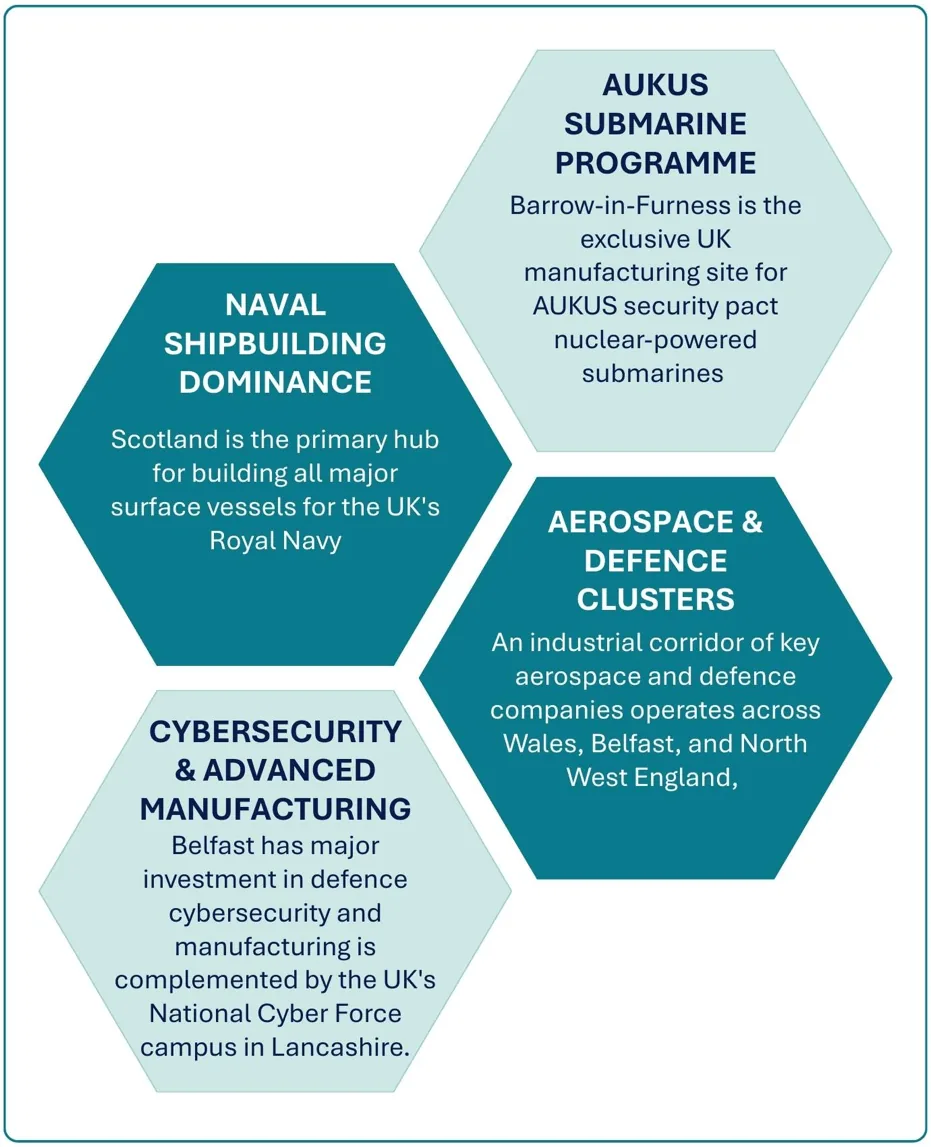

DEFENCE AND SECURITY: TOWARDS A “SAFE LAKE”

The Irish Sea's strategic importance is underscored by its role in national and international defence, most notably through the Australia-UK-US (AUKUS) security pact. The region is home to critical defence assets and industries. Scotland dominates the UK's shipbuilding of all major surface naval assets for the Royal Navy[31], while Barrow-in-Furness is the sole site for building nuclear-powered submarines for the Royal Navy and for the AUKUS partners[32]. Wales, Belfast and the North West of England are home to multiple key companies operating in the Aerospace industry, with Ireland’s focus on simulation software, drones, and dual-use technologies.

The Irish Sea's strategic importance is underscored by its role in national and international defence, most notably through the Australia-UK-US (AUKUS) security pact. The region is home to critical defence assets and industries. Scotland dominates the UK's shipbuilding of all major surface naval assets for the Royal Navy[31], while Barrow-in-Furness is the sole site for building nuclear-powered submarines for the Royal Navy and for the AUKUS partners[32]. Wales, Belfast and the North West of England are home to multiple key companies operating in the Aerospace industry, with Ireland’s focus on simulation software, drones, and dual-use technologies.

As part of the UK's Modern Industrial Strategy, Belfast's defence sector is receiving significant investment to foster growth and create jobs. This includes a dedicated Defence Growth Deal for Northern Ireland, backed by a £250 million fund, to build on the city's strengths in cybersecurity and advanced manufacturing, reinforcing Belfast's role as a key hub for the UK's defence industry.

Such a shared concentration of defence capability naturally comes with both threats and opportunities. Russian spy ships regularly patrol near undersea cables; military exercises were also conducted off the Irish coast[33]. In 2025, the UK-Ireland defence agreement’s discussions have intensified[34], especially because both nations recognise undersea cables as a mutual vulnerability.

There are two key Defence and Security Clusters in the Irish Sea Rim Geography, these are the North West Regional Defence & Security Cluster (NWRDSC) and the South West Regional Defence & Security Cluster (SWRDSC). These clusters engage with defence in the Irish Sea.

Belfast's defence sector is receiving UK's Modern Industrial Strategy investment manufacturing and cybersecurity, include a £1.6 billion contract for Thales and substantial funding for the modernisation of Harland & Wolff's shipyard.

The Irish Sea Rim provides the soft infrastructure (relationships, forums, shared interests) that could eventually support harder security cooperation. The Irish Sea Rim will initially strengthen the Irish Sea as shared economic and collaborative space, which could naturally evolve into a shared security space - essentially achieving a "Safe Lake" status for the Irish Sea regions.

SPECIALISED HUBS

CREATIVE AND SCREEN:

- The Isle of Man has successfully leveraged its unique status to become a global hub for eGaming. The sector contributes over 10% of the island's economy[35].

- The screen industries in Scotland produce £315 million GVA annual and, with committed investment and development by Screen Scotland, aims to reach £1billion GVA by 2030. With strong creative and screen clusters across Glasgow and Stirling and BFI-funded initiatives such as the Stornoway Studio Training Programme and Reset, which supports people retraining in the animation, VFX and gaming sectors, growth is on track to reach these economic goals.

- The Welsh creative sector is a significant and rapidly growing part of its economy, contributing over 5% to the Welsh GDP. The industry is diverse, with major strengths in film and television production, a rising games industry, and a strong music and publishing scene. Supported by the Welsh Government's "Creative Wales" agency, the sector has attracted major international productions, fostering job creation and solidifying Wales's reputation as a global creative hub

- Northern Ireland has seen significant growth in studio space in recent years with a mixture of purpose-built studios and alternative build space for productions, such as Belfast Harbour Studios, Titanic Studios and Loop Studios in the Belfast City Region.

CLIMATE TECH:

The UK leads a £42billion ClimateTech sector with growing hubs in Manchester and Glasgow’s city regions as hubs for investment. ClimateTech focused on innovation responses to climate change, reducing emissions and enhancing sustainability with focus on clean energy, the built environment, agriculture and food production and carbon markets.

These sectors map directly onto areas with the highest projected growth and, linking to rural and coastal assets, provides promise and investment in places outside the Irish Sea Region’s largest city-regions. With a UK ClimateTech All-Party Parliamentary Group launched in December 2024, there is ample opportunity to connect policy, public and private investment to accelerate innovation across the Irish Sea Region, focusing investment conversations in major cities with the innovation delivery, skill and workforce development rooted in the regions’ wider towns, rural and coastal areas.

LIFE SCIENCES:

The UK and Ireland hold some of the major global life sciences clusters with ample opportunities for connected innovation, investment and impact – across devolved nations and internationally. Five of the seven major UK life sciences cluster organisations are part of the Irish Sea Region geography including:

- The Northern Heath Science Alliance, NHSA: The north of England, with a major cluster corridor from Liverpool City Region, through Cheshire and into Greater Manchester

- Nine of the top ten international pharmaceutical companies are based in Ireland

- The South West of England, which holds the 3rd fastest growing life sciences sector in the UK

- Health Innovation Research Alliance Northern Ireland, HIRANI: Northern Ireland, which brings 17 research organisations and 300 companies together to generate over £1.1 billion GVA

- NHS Research Scotland, across the Glasgow-Edinburgh Corridor

- Life Science Hub Wales, which supports 12,000 jobs across 250 companies.

The Irish Sea Rim presents opportunities for significant connection between the powerful pharmaceutical mass production industry in Ireland, and the UK’s strength in new drug discovery, and this is something we will explore with key stakeholders and partners.

SCIENCE PARKS:

The Irish Sea region is also home to a substantial concentration of science parks (Figures 6.9-6.15), highlighting the scale and breadth of innovation within the region. Harnessing the power of this infrastructure through the Irish Sea Rim’s ability to connect, bridge, and amplify innovation, skills development, and supply chains will both complement those in London and the Greater South East, and create a powerful scientific and economic counterbalance. This in turn will maximise the UK and Ireland’s global leadership in this area.

M-SPARC Science Park, Wales. Image Credit: Irish Sea Rim

Figure 6.9: North West England Science Parks

Location

Name

Focus

Size

Logo

Website

Cheshire

Alderley Park

A world-leading science and tech campus including Life Sciences and Pharmaceuticals

400 acres

Runcorn, Cheshire

The Heath Business and Technical Park

Serviced labs; tech; office space

>120 businesses

Liverpool

Liverpool Innovation Park

A business park offering high quality, well-connected office space.

Liverpool

Liverpool Science Park

A specialist science and tech cluster of over 60 businesses. The Park offers coworking space, serviced offices and leased office and lab space, meeting rooms, and event space.

>60

businesses

Manchester

Manchester Science Park

The Park is home to an innovation community of some of the region's most disruptive, fast-growing science and tech businesses.

>150 businesses

Warrington, Cheshire

Sci-Tech Daresbury

Part of the Science and Technology Facilities Council Science Campus. A technology business community.

Moor Row, Cumbria

Westlakes Science & Technology Park

Nuclear; R&D; Energy

Figure 6.10: Wales Science Parks

Location

Name

Nature

Size

Logo

Website

Anglesey

Menai Science Park (M-Sparc)

Owned by Bangor University, this was Wales’ first science park

Cardiff

Cardiff Edge

A Life Sciences R&D site, part of Pioneer Group

Figure 6.11: South West England Science Parks

Location

Name

Nature

Size

Logo

Website

Emersons Green, Bristol

Bristol and Bath Science Park

Includes a Carbon Fibre Research Centre, part of the High Value Manufacturing Catapult initiative; an “innovation centre” for new business and “grow on centre” for subsequent expansion.

59 acres

Bristol Meeting Rooms & Offices | Bristol & Bath Science Park

Paignton, Devon

Electronics and Photonics Innovation Centre

Microelectronics, Photonics, MedTech, AgriTech, MarineTech, and Aerospace Innovation and technology

Exeter

Exeter Science Park

A hub for Innovation and entrepreneurship. Businesses in science, technology, engineering, maths and medicine (STEMM)

64 acres

University of the West of England, Stoke Gifford, Bristol

Future Space

Facilities for R&D in advanced engineering, health & life sciences, digital and green tech.

Future Space | Innovative Workspace for Science & Technology Businesses | Bristol

Plymouth

Plymouth Science Park

Multi-sector hub including digital, tech and life sciences. Offers office accommodation, wet and dry laboratory space

25 acres

Plymouth Science Park | Office Space | Science & Technology | Meetings

Porton, Wiltshire

Porton Down and Porton Science Park

Part of the Science and Technology Facilities Council Science Campus. A science and defence technology, health and life science business community.

7,000 acres

Wet Labs and Office Space for Rent in Wiltshire, England | Porton Science Park

Figure 6.12: West Scotland Science Parks

Location

Name

Nature

Size

Logo

Website

Glasgow

BioCity Glasgow

The biotech incubator has an assortment of fully accessible, contemporary offices and lab space to rent.

20 acres

East Kilbride

Scottish Enterprise Technology Park

A centre of technology excellence

34 hectares

Glasgow

West of Scotland Science Park

A hub for a wide range of companies from life sciences and technology sectors including ultrasonics, pharmaceuticals, mobile computing, clean rooms, satellites, laser systems, telecommunications, pre-clinical drug discovery and optoelectronics.

60 acres

West of Scotland Science Park | Innovative Science Businesses

Oban

European Marine Science Park (EMSP)

The EMSP s a world-class, multi-purpose facility for marine science research and blue economic business growth

Figure 6.13: Northern Ireland Science Parks

Location

Name

Nature

Size

Logo

Website

Belfast and Londonderry

Catalyst

A science and technology hub focused on fostering innovation and entrepreneurship

Belfast

Northern Ireland Advanced Composites and Engineering Centre

A technology hub for the research and development of advanced engineering and advanced materials technologies across a range of industrial sectors

http://www.niace-centre.org.uk/

Belfast

Momentum One Zero

Part of Queen’s University, Belfast, it is a new global innovation centre which aims to bring Secure Connect Intelligence expertise into key sectors - Digital Health, Agri-food, and Cyber Security, exploring applications to Semiconductor Security, Space, FinTech & Net-Zero.

Belfast

Advanced Manufacturing Innovation Centre

The Advanced Manufacturing Innovation Centre, led by Queen's University Belfast, is key to future manufacturing in Northern Ireland, as an industry-led, open-access manufacturing and engineering innovation centre with state-of-the-art facilities, underpinned by academic excellence.

Belfast

Centres funded under the City Deal

Studio Ulster, Centre for Connected Health Care Technologies, UK National Digital Twin Centre, and I-REACH clinical Labs centre

Figure 6.14: Ireland Science Parks

Location

Name

Nature

Size

Logo

Website

Cavan

Cavan Business and Technology Park

A business park to suit the needs of both manufacturing and international services sectors.

37 acres

Dublin

Nova UCD (University College Dublin)

Nova UCD, nurture and support high-tech and knowledge-intensive spin-in and spin-outs

Nexus UCD, the Industry Partnership Centre, provide high-quality office space,The AgTech UCD Innovation Centre, , is supporting and accelerating early-stage start-ups and SMEs with disruptive technologies in the AgTech, agrifood and veterinary sectors

Shannon Airport

Shannon Campus West and East Zone

Zone is now one of Ireland's largest multisectoral business parks, which hosts the highest concentration of FDI companies outside of Dublin.

Shannon holds a strategic location, serving as the link between Galway and Limerick, providing entry to the Mid-West Region.

600

https://snnairportgroup.ie/commercial-property/our-business-park/

Figure 6.15: Isle of Man Science Parks

Location

Name

Nature

Size

Logo

Website

Ramsey

Mountain View Innovation Centre

We’re all about nurturing innovation at Mountain View –sharing physical space with fellow businesses and providing a creative environment in which to turn good ideas into successful enterprises in a stimulating, supportive environment.

25 acres

https://mvic.im/