PRODUCTIVITY AS THE CORE GROWTH CHALLENGE

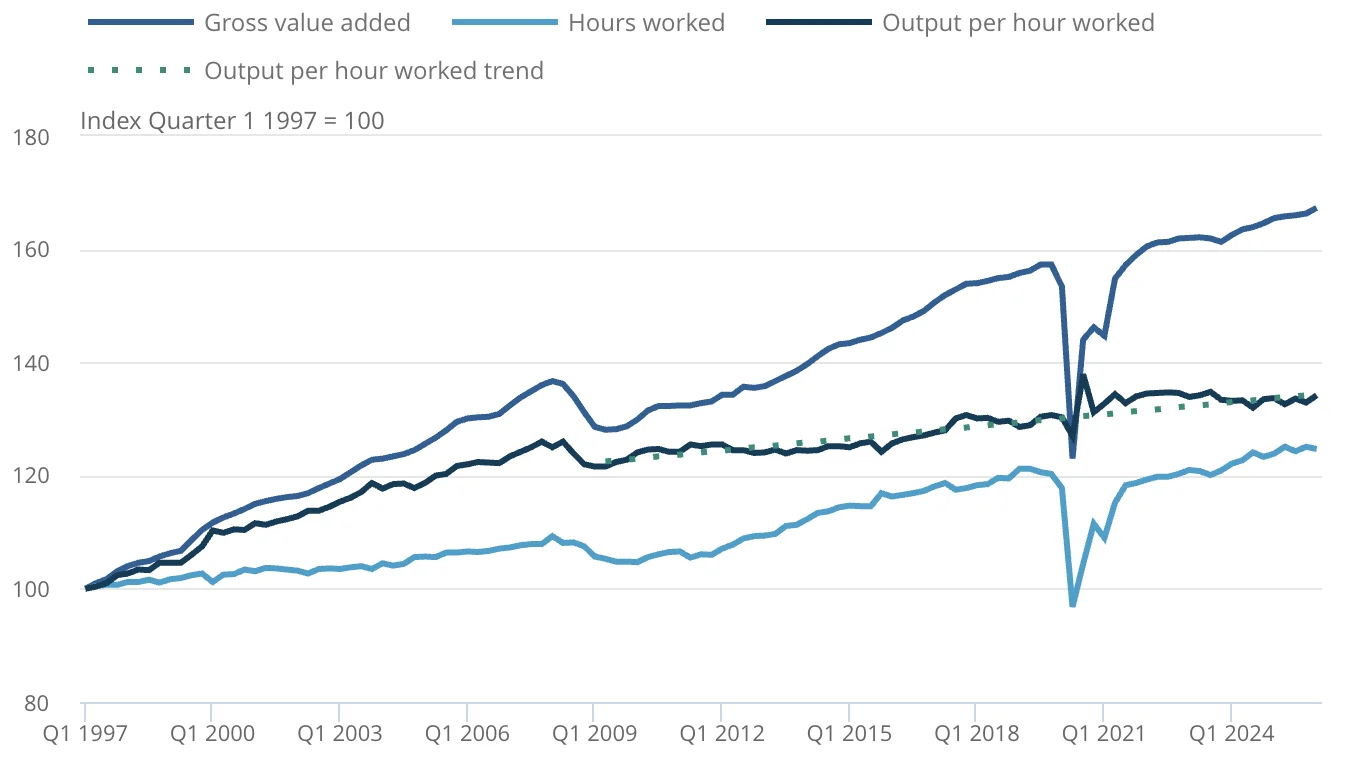

Productivity is the fundamental driver of long-term living standards, real wage growth, business competitiveness and fiscal sustainability. It measures how effectively an economy converts labour, capital, infrastructure, knowledge, technology, data and institutional capability into higher-value output. For the Irish Sea Rim, productivity is not an abstract economic indicator; it is the core test of whether the region can generate better jobs, stronger firms, more resilient trade, higher wages, cleaner growth and more sustainable public finances. However, according to the Office for National Statistics, while UK productivity for the first quarter of 2026 was 3.5% above the 2019 average level, productivity growth, in terms of output per hour worked, remains weak compared with pre-2008 trends (figure 16.1)[57].

Across the UK, Ireland and the Isle of Man, productivity is now central to government economic strategy. The UK’s Modern Industrial Strategy is a ten-year plan to increase business investment and grow future-facing sectors, including advanced manufacturing, clean energy industries, creative industries, defence, digital and technologies, financial services, life sciences, and professional and business services. Ireland’s Action Plan on Competitiveness and Productivity sets out 85 actions, including 26 priority actions, covering research, innovation and skills; FDI and exports; SME creation and scaling; regulation and costs; infrastructure delivery; and sustainable business and regional development[58]. Northern Ireland’s economic vision is explicitly structured around Good Jobs, Raising Productivity, Decarbonisation and Regional Balance[59]. Scotland’s National Strategy for Economic Transformation identifies increasing productivity as one of five transformational programmes, alongside entrepreneurship, new markets, skills and fairer opportunity[60]. The Isle of Man’s economic strategy links growth to productivity, investment, innovation, population, jobs and GDP growth[61].

The strategic relevance of the Irish Sea Rim is that these priorities overlap geographically, economically and politically around the Irish Sea. The region contains ports, freeports, universities, logistics corridors, clean energy assets, advanced manufacturing clusters, digital and cyber capability, maritime industries, professional services, island-economy specialisms and significant SME populations. However, these assets are fragmented across national, devolved, regional and island jurisdictions. The Irish Sea Rim productivity opportunity is therefore to connect complementary assets into a functional transnational economic system: a unified Investment, Innovation and Enterprise Zone that treats the Irish Sea as shared economic infrastructure rather than as an administrative boundary.

THE MACRO PRODUCTIVITY PICTURE: UK, IRELAND, AND ISLE OF MAN

The productivity challenge is structurally different across the UK, Ireland and the Isle of Man.

The UK faces a long-running productivity slowdown and a deep spatial imbalance. The latest ONS productivity flash estimate shows that UK output per hour worked in Q1 2026 was 3.5% above its 2019 average level and 0.4% higher than Q1 2025. However, ONS also states that productivity growth remains weak compared with trends before the 2008 global financial crisis. This is the core UK productivity puzzle: the economy is producing growth, but not at the efficiency trajectory needed to drive sustained wage growth and fiscal resilience.

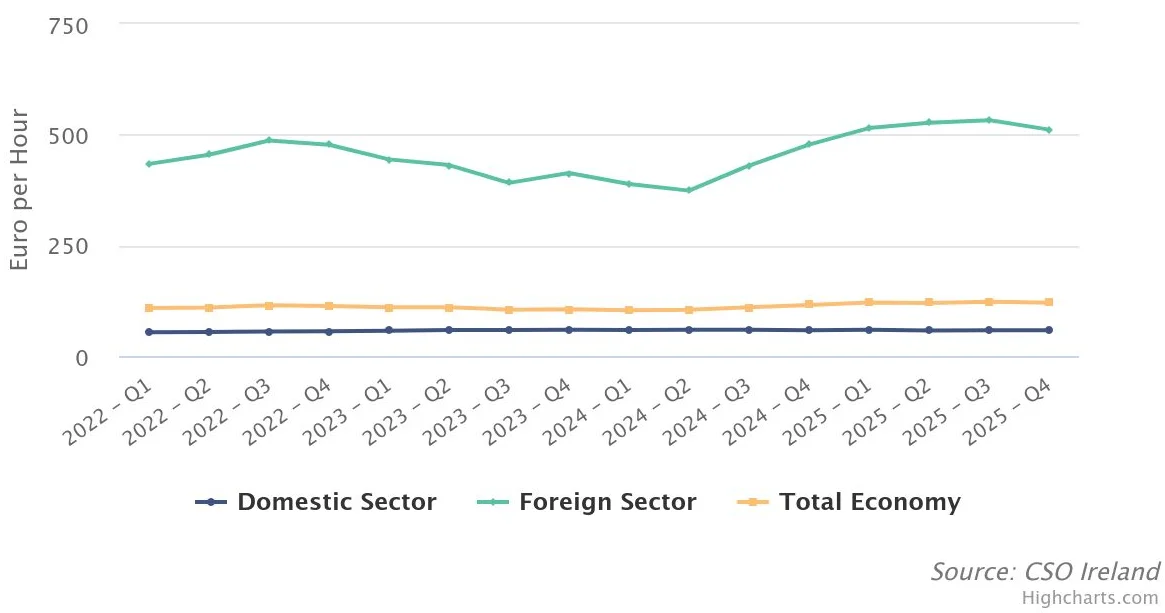

Ireland presents a different productivity profile. Headline Irish productivity is very high, but it is heavily shaped by foreign-owned multinational enterprise activity. In Q4 2025, Ireland’s total economy labour productivity was €120.50 per hour, but domestic-sector productivity was €58.20 per hour, while foreign-sector productivity was €511.40 per hour (figure 16.2). CSO Ireland therefore prioritises the domestic sector for analytical purposes because of the considerable influence of the foreign sector on total-economy measures[62]. Ireland’s productivity challenge is therefore a dual-economy challenge: sustaining world-leading multinational performance while strengthening productivity, scaling and innovation diffusion across indigenous and domestic firms.

The Isle of Man represents a third model: a small, high-income, service-dominant island economy with high-value specialisation but acute scale constraints. In 2023/24, insurance accounted for 16.9% of the Isle of Man economy, eGaming for 14.2%, and professional services for 13.8% [63]. This supports a high-value economic model, but also creates exposure to sector concentration, labour supply constraints, housing pressures, digital infrastructure needs and external income flows. For the Isle of Man, the productivity challenge is not about scale in the conventional sense, but about maximising value from a finite workforce and connecting specialist capability into wider markets.

These three models create a strong case for the Irish Sea Rim. The UK needs stronger regional productivity beyond London and the South East. Ireland needs wider productivity spillovers into domestic and regionally embedded enterprise. The Isle of Man needs routes to scale specialist capabilities through partnership rather than volume. The Irish Sea Rim can address all three by connecting firms, ports, supply chains, universities, investors, skills systems and innovation assets across the Irish Sea.

REGIONAL PRODUCTIVITY AND THE IRISH SEA OPPORTUNITY

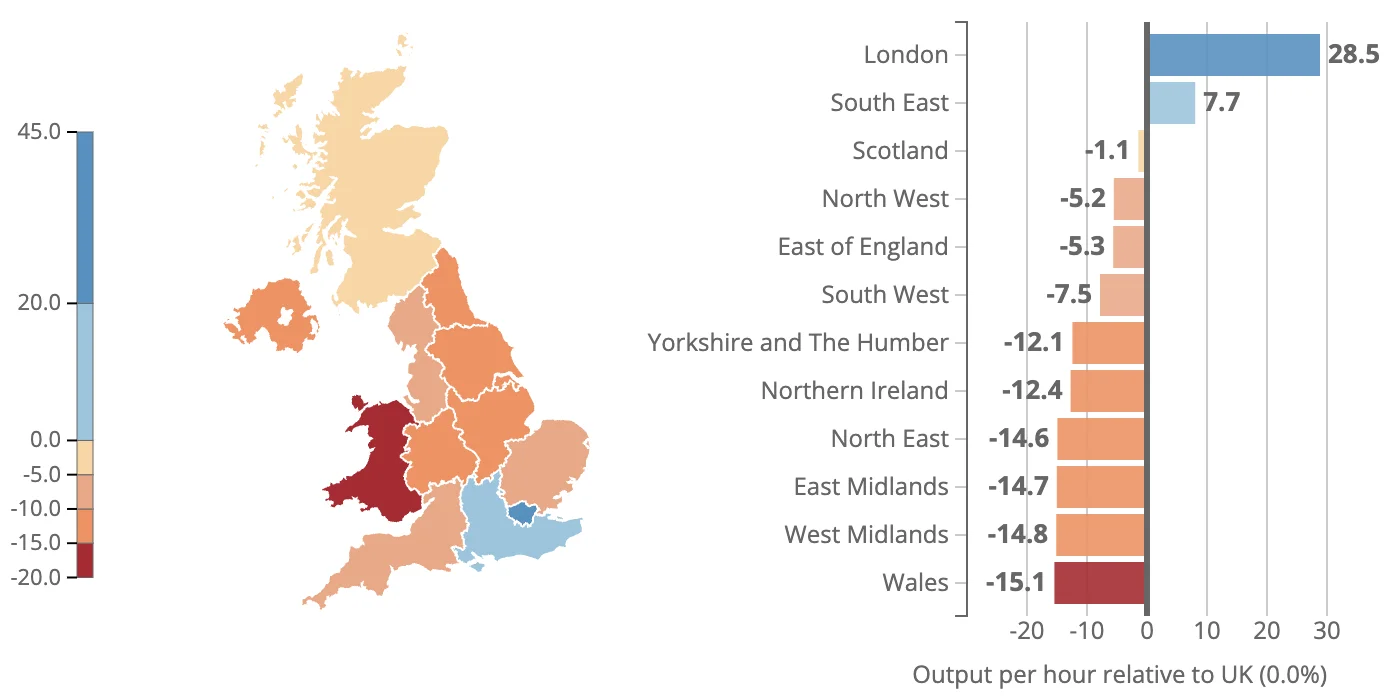

The UK productivity problem is also a regional systems problem. ONS regional productivity data show that, in 2023, London’s output per hour worked was 28.5% above the UK average and the South East was 7.7% above the UK average. Every other UK country and English region was below the UK average. Wales, the West Midlands, the East Midlands and the North East had the four lowest output-per-hour levels, at 15.1%, 14.8%, 14.7% and 14.6% below the UK average respectively[64] (figure 16.3).

This matters directly to the Irish Sea Region. Wales had GVA per hour worked at 84.9% of the UK average in 2023, the lowest of the UK countries and English regions[65]. Northern Ireland remains below the UK average but has placed productivity improvement at the centre of its economic vision. The North West and South West of England remain below the UK average on productivity levels, but contain major assets in ports, advanced manufacturing, clean energy, logistics, digital, life sciences, universities, professional services and freeport activity. Scotland sits closer to the UK average than several other UK regions, but its national economic strategy still identifies productivity as a core transformation priority.

Source: Regional Productivity from the Office of National Statistics[66]

There are also important signs of momentum around the Irish Sea. ONS data show that the North West made the largest positive contribution to UK output-per-hour growth in 2023 compared with 2019 and had the strongest cumulative average annual growth rate of any UK region between 2019 and 2023, at 2.4% compared with 0.7% for the UK as a whole[67]. This is strategically significant because North West England is one of the Irish Sea Rim’s central productivity anchors. Liverpool, Manchester, the M62 corridor, the Liverpool City Region Freeport, advanced manufacturing, nuclear, hydrogen, health innovation, materials, logistics, ports, universities and professional services together form a powerful but still under-connected productivity platform.

The ISR proposition is therefore not that the Irish Sea Region lacks productive assets. It is that these assets are not yet sufficiently connected into a coherent economic system. The productivity opportunity lies in improving the connectivity, scale, visibility and interoperability of the region’s assets so that firms can access larger markets, universities can collaborate across borders, ports can function as intelligent logistics nodes, and SMEs can participate in higher-value supply chains.

THE IRISH SEA RIM AS A PRODUCTIVITY PLATFORM

The Irish Sea Region comprises South West Scotland, North West England, Wales, the Great South West of England, Northern Ireland, Ireland, and the Isle of Man. It is not a single administrative economy, but it is a coherent functional economic geography. Its productivity potential lies in the interaction between complementary assets.

South West Scotland brings maritime, rural innovation, clean energy, food, ports, tourism and environmental assets. North West England provides major productivity anchors through Liverpool, Manchester, the M62 corridor, the Liverpool City Region Freeport, advanced manufacturing, nuclear, hydrogen, health innovation, materials, logistics, ports, universities and professional services. Wales brings ports, freeports, marine energy, compound semiconductors, cyber security, advanced manufacturing, agri-food and university assets, while also facing acute productivity gaps. The Great South West contributes clean energy, aerospace, defence, marine engineering, environmental science, food, farming, natural capital and coastal innovation. Northern Ireland brings advanced manufacturing, cyber, fintech, agri-food, logistics, life sciences and a distinctive position between the UK internal market and the EU-facing Irish economy. Ireland adds multinational investment, domestic enterprise, research capability, export orientation, ports, energy, data and advanced services. The Isle of Man adds specialist financial, digital, regulatory and island-economy capability.

The purpose of the Irish Sea Rim is to create an Investment, Innovation and Enterprise Zone connecting the six jurisdictions around the Irish Sea Rim, with a wider model built around prosperity, innovation, cross-border business networks, research partnerships, sustainable energy and regional collaboration. In productivity terms, this is best understood as a platform proposition: the Irish Sea Rim can create the connective tissue that enables the region’s assets to operate at greater scale.

Trade and logistics are the most immediate opportunity. The UK Government’s Ireland trade and investment factsheet reports total UK–Ireland trade in goods and services of £89.3bn in the four quarters to the end of Q4 2025, an increase of 5.6% in current prices compared with the previous year. UK exports to Ireland were £56.4bn and UK imports from Ireland were £32.9bn; Ireland was the UK’s sixth largest trading partner, accounting for 4.7% of total UK trade[68]. These flows already constitute a major productivity corridor. However, post-Brexit trade conditions, customs requirements, regulatory divergence, port capacity, documentation burdens, cyber risk and fragmented digital systems can add time, cost, uncertainty and duplication.

The Irish Sea Rim addresses this through smart trade and logistics infrastructure: bonded logistics corridors, smart port data-sharing, trusted trader models, digital customs processes, interoperable trade documentation, real-time seal integrity, cyber-secure freight systems, coordinated freeport links and better integration with road and rail corridors such as the M62 and trans-Pennine routes. The outcomes of this are not just to improve transport efficiency, but to raise the productivity of firms whose business models depend on speed, reliability, compliance, inventory control and supply-chain resilience.

ECONOMIC ENGINES AS A DRIVER OF PRODUCTIVITY

The Irish Sea Rim’s productivity additionality comes through six practical mechanisms.

- REDUCE TRADE FRICTION: Align ports, freeports, customs systems, freight data, cyber security, trusted trader models and bonded logistics.

- ACCELERATE INNOVATION DIFFUSION: Enable SMEs to access applied research, demonstrators, university expertise, procurement opportunities, investment networks and testbeds across the whole region rather than only within their local geography.

- DEEPEN LABOUR-MARKET PRODUCTIVITY: Support shared skills programmes in maritime logistics, customs, cyber security, AI, green energy, advanced manufacturing, food systems, health innovation and visitor economy productivity.

- SUPPORT CLEAN GROWTH: Connect offshore wind, floating wind, marine energy, hydrogen, nuclear, geothermal, green shipping, port decarbonisation and energy-system innovation.

- CREATE INVESTABLE SCALE: Bundle fragmented local projects into larger transnational portfolios.

- STRENGTHEN INCLUSIVE REGIONAL GROWTH: Link high-value innovation activity to coastal, rural and peripheral communities.

Clean growth is one of the strongest ISR productivity opportunities. The Great South West Clean Energy Powerhouse Prospectus identifies major opportunities including GW-scale floating offshore wind in the Celtic Sea, Hinkley Point C, geothermal power, solar, onshore wind, tidal and wave energy, hydrogen and biofuel production and storage, critical minerals, and battery production and storage. It states that the Great South West has the potential to supply up to 11% of Great Britain’s clean power demand by 2035, unlocking up to £10bn in GVA and 175,000 jobs[69]. Through ISR, these assets could be connected to Welsh ports and freeports, Northern Irish engineering and maritime capability, Irish ports and energy systems, Scottish clean energy strengths, North West industrial corridors and Isle of Man finance and regulation.

The Irish Sea Rim’s Economic Engines will therefore work as productivity platforms, via interlinked programmes that convert regional assets into measurable outcomes. Priority Economic Engines include Smart Trade and Bonded Logistics; Clean Maritime and Green Shipping; Offshore and Marine Energy; Digital, AI and Cyber Assurance; Advanced Manufacturing and Resilient Supply Chains; Food, Farming and Blue Economy Innovation; Health and Life Sciences; and Coastal Visitor Economy Productivity. Each will be measured through output per hour where available, GVA per job, business investment, export growth, innovation adoption, SME participation, private investment leveraged, freight reliability, skills participation, higher-value job creation and reduced trade friction.

THE IRISH SEA RIM AS A STRATEGIC PRODUCTIVITY FORCE MULTIPLIER

The Irish Sea Rim can act as a productivity force multiplier for the UK, Ireland and the Isle of Man. Its role is not to replace national, devolved or regional strategies, but to connect them where their priorities already overlap via growth, innovation, trade, infrastructure, clean energy, skills, investment and inclusive regional development.

The evidence shows both the scale of the productivity challenge and the scale of the opportunity. UK productivity remains weak by historic standards and spatially uneven. Ireland’s productivity is strong but dualistic. Wales and parts of the Irish Sea periphery face deep productivity gaps. Northern Ireland and the North West show opportunities for productivity momentum. The Isle of Man requires specialist scale and resilience. UK-Ireland trade already exceeds £89bn a year, but remains exposed to friction, delay and system fragmentation.

The Irish Sea Rim proposition reframes this challenge. It turns the Irish Sea from an administrative boundary into shared economic infrastructure. By connecting ports, freeports, logistics corridors, universities, SMEs, clean energy assets, industrial clusters, digital capability, island economies and investment platforms, the Irish Sea Rim can create the conditions for agglomeration, knowledge spillovers and productivity diffusion. This is the core additionality of a unified, transnational Investment, Innovation and Enterprise Zone – raising productivity not by concentrating growth in one place, but by connecting complementary assets across the whole region. In doing so, the Irish Sea Rim can support sustainable, inclusive growth; strengthen UK-Ireland trade resilience; improve productivity in coastal, rural and peripheral communities; and create a vital economic complement and counterbalance to London and the Greater South East.