The Economic and Innovation Landscape

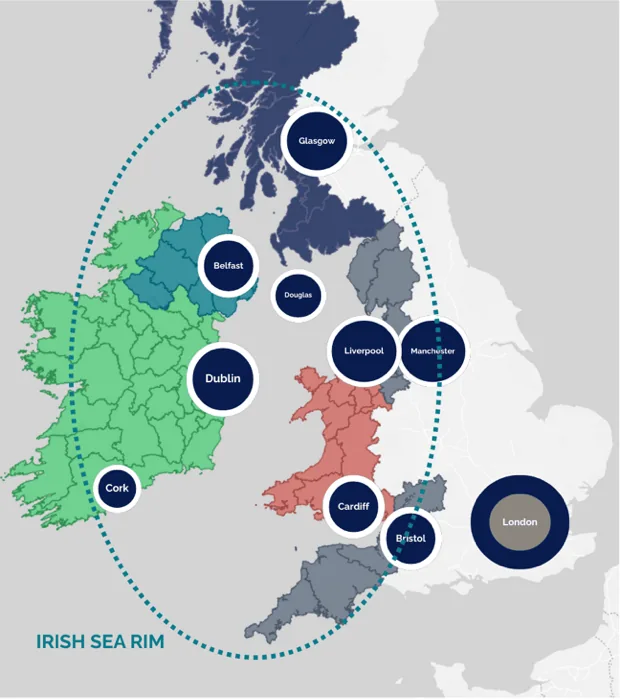

The Irish Sea Rim is a thriving area of economic activity, encompassing major city regions including Glasgow, Liverpool, Manchester, Bristol, Cardiff, Belfast, Dublin, and Cork. The region is well-defined and has sufficient closeness to allow face-to-face collaboration. Together the Irish Sea Region has a powerful critical mass, alongside diverse, yet complementary research and innovation centres of excellence.

THE NEED FOR GREATER REGIONAL ECONOMIC BALANCE

London is a global economic powerhouse and investment centre, far outstripping any other region within the UK. The economic health of London is critical to the UK, as its GDP far outstrips any other UK city, even Manchester, which is consistently described one of the fastest growing cities in Europe. As part of the Greater South East (London, South East England and the East of England), London is a significant draw for national and global investment and talent.

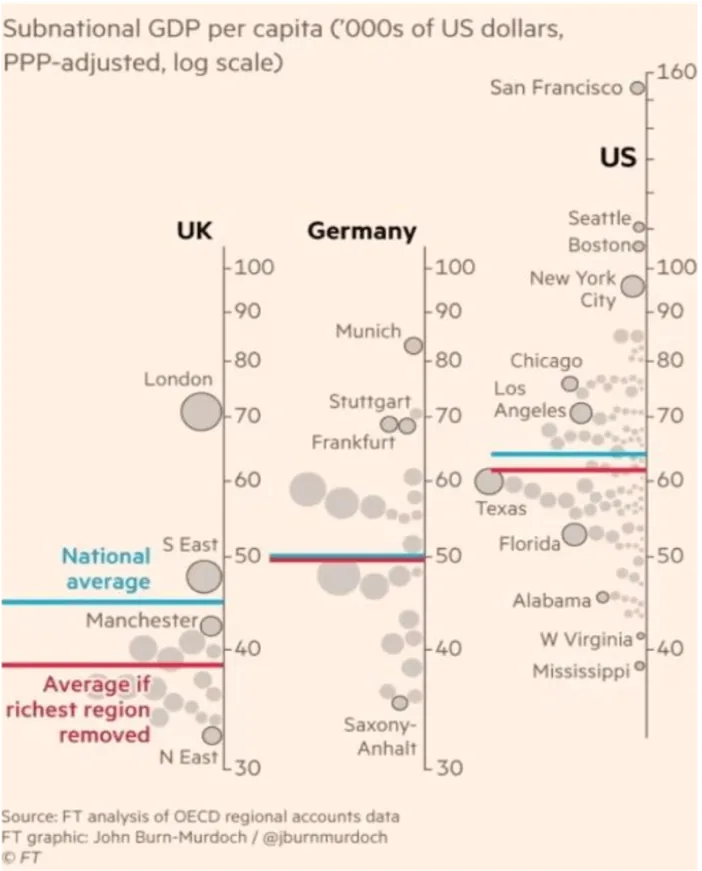

Yet such intense financial concentration in a single area creates significant vulnerability for the UK economy. According to data from the Organisation for Economic Cooperation and Development (OECD), the UK is characterised by a significant regional economic imbalance compared with other OECD countries, including the United States, Germany, and the Netherlands [47]. Figure 15.1 highlights the relative regional economic concentration compared with Germany and the United States. This figure also indicates that the impact of a significant economic or environmental shock to London could be catastrophic for the rest of the UK.

As a region, London and the Greater South East face significant challenges. The core economy of this region is dominated by the global financial services hub within London, with a focus on high growth, high tech in the rest of the region. Environmentally, the region is vulnerable to environmental changes, with water scarcity an increasing problem, and flooding from increasing sea levels a major risk to the City of London.

While no single UK city can create the stability to put the UK on a par with more economically diverse nations, a high-level summary comparison indicates that, together, the combined cities and regions comprising the Irish Sea Rim both complement and create a powerful economic and innovation complement and counterweight to London and the Greater South East (Figures 15.2 and 15.3).

Figure 15.2: High-level summary comparison: Irish Sea Region vs Greater South East

Metric | Irish Sea Rim | Greater South East |

Approx Population | ~23.6 million | ~24.8 million |

Approx GDP (GVA) | ~£930 billion | ~£1.09 trillion |

Approx Businesses | ~1.0 million | ~1.3 million |

Universities | 55-60 | 65-70 |

Student Population | ~1.2 million | ~1.2 million |

Academic Staff | ~130,000 | ~120,000 |

In addition, the regional economies comprising the Irish Sea Rim are more diverse and distributed, with strengths in a wide mix of industries, including technology, advanced manufacturing, maritime transport and logistics, life sciences, and energy (including renewable). Through its climate and natural environment, the region has a more stable water supply and access to renewable energy. In recent years, the Irish Sea Rim has been regarded increasingly as a desirable place to live and work, while globally it is seen as a safe place for trade in the light of increasing global volatility and uncertainty.

Figure 15.3: Regional influence of cities around the Irish Sea Rim compared with London

The economic comparison should be viewed within the context of research and innovation investment. Traditionally, the Irish Sea Rim has received significantly less investment than London and the Greater South East (see below). Formally establishing the unified, cross-border Irish Sea Rim Investment, Innovation, and Enterprise Zone, and targeting investment into its industries and regions therefore creates an unprecedented opportunity for delivering non-linear returns on investment in terms of sustainable, inclusive economic growth.

IRISH SEA RIM CITIES ECONOMIC OVERVIEW

The economic geography of the Irish Sea Rim is dominated by several powerful urban hubs that serve as the primary engines of growth and innovation. These cities have largely navigated the transition from industrial pasts to futures grounded in knowledge-intensive sectors, attracting investment and talent. However, this narrative of success coexists with underlying structural weaknesses, including persistent productivity gaps and wage disparities, which hint at a more complex reality.

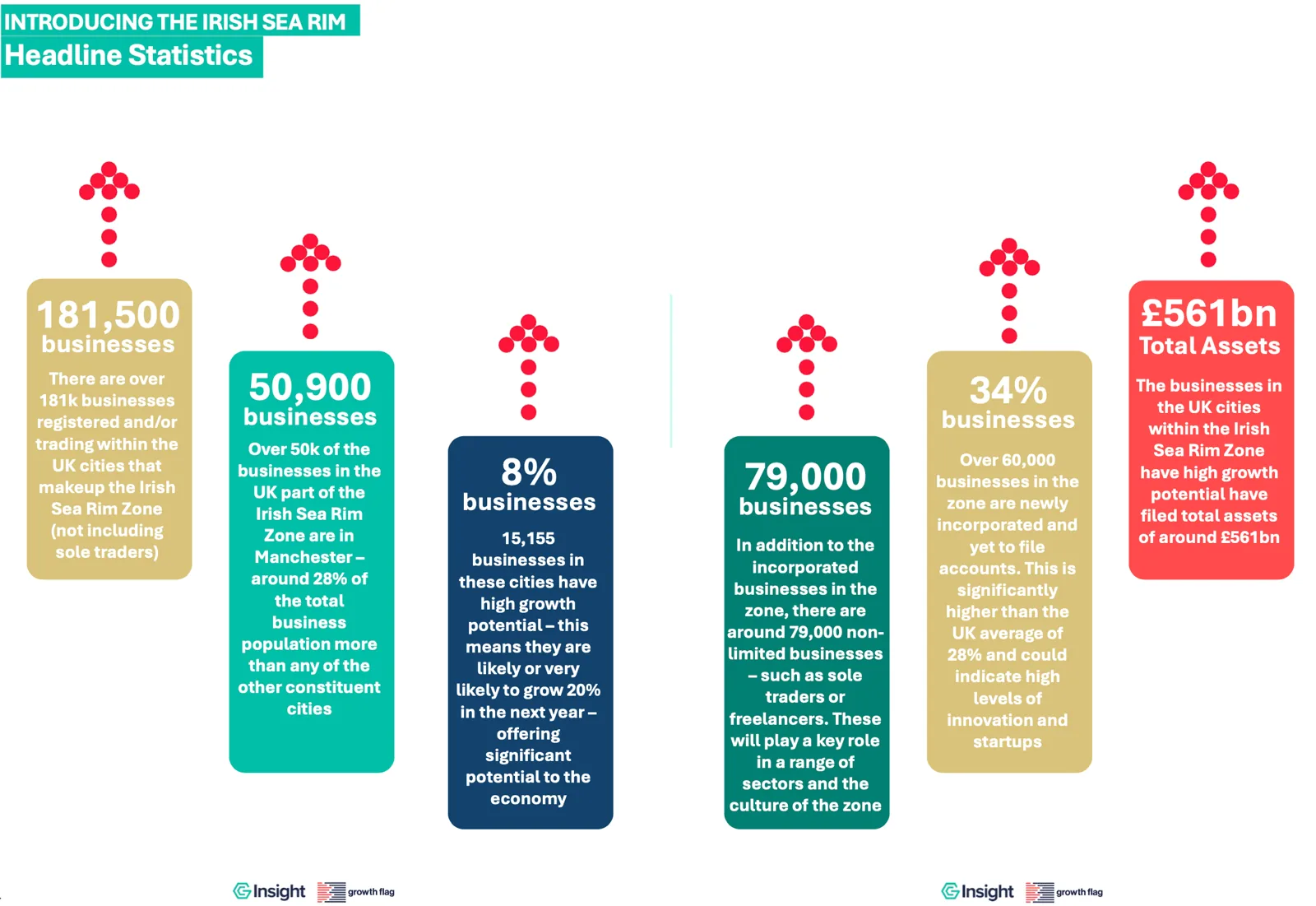

A snapshot business analysis of the six UK cities around the Irish Sea Rim (Glasgow, Liverpool, Manchester, Cardiff, Bristol, and Belfast) was carried out by GC Insight using Growth Flag, their proprietary data tool. This analysis provides insights into the size, health and growth of the business base in these cities and supports the further development of the Irish Sea Rim Investment, Innovation, and Enterprise Zone and its associated projects (Figure 15.4).[48]

Key takeaways include:

- There are over 181,000 businesses actively registered and or trading in the key UK cities of the Irish Sea Rim: These businesses are spread across the zone, offering significant economic opportunities. Beyond these businesses, there are at least a further 79,000 non-limited businesses within these UK cities (such as sole-traders and freelancers) while the wider zone around these cities is home to many more businesses

- Businesses in these cities are generally in strong financial health, and there are many more new businesses here than the UK average: Around 34% of businesses in these cities are newly incorporated and yet to file accounts, compared with 28% in the UK overall. This could indicate strong levels of innovation and startups, supporting the aims of the Irish Sea Rim.

- Over 15,000 businesses in the zone have high growth potential: These businesses are likely or very likely to grow by 20% over the next year and could offer significant economic returns for the zone and its local communities if supported to achieve this growth (Figure 15.5).

While most businesses in the Irish Sea Rim are in strong financial health, some exhibit signals of financial risk: Nearly 20,000 businesses within the eight cities demonstrate some signals of financial distress, with over 1,000 of these showing critical signs. Understanding the landscape of business health and risk will be important for developing support and programmes that can drive productivity and economic growth throughout the Irish Sea Rim

While most businesses in the Irish Sea Rim are in strong financial health, some exhibit signals of financial risk: Nearly 20,000 businesses within the eight cities demonstrate some signals of financial distress, with over 1,000 of these showing critical signs. Understanding the landscape of business health and risk will be important for developing support and programmes that can drive productivity and economic growth throughout the Irish Sea Rim - 99.5% of businesses within the cities are small or medium enterprises with under 250 staff: With 870 large businesses.

- Businesses in the Irish Sea Rim cities have a range of international links: Including through directors of foreign nationality and through parent / group companies located in foreign countries outside the UK.

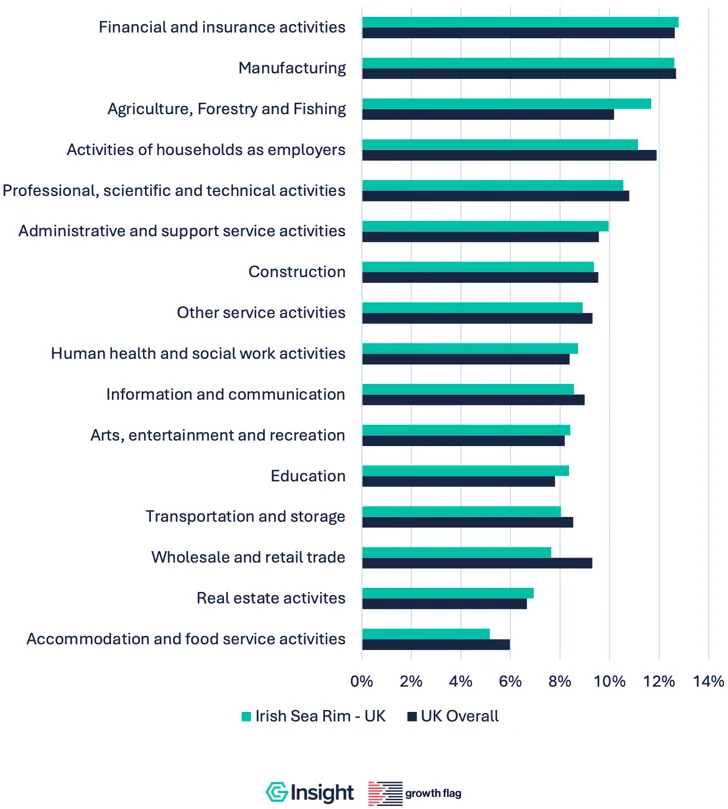

Figure 15.5: Percentage of businesses with high growth potential by sector

We will continue to work with GC Insights as a partner to undertake wider high-level analyses of the Irish Sea Rim, with focussed reports providing insights on the unique strengths and challenges of the Irish Sea Rim overall, and its constituent regions.

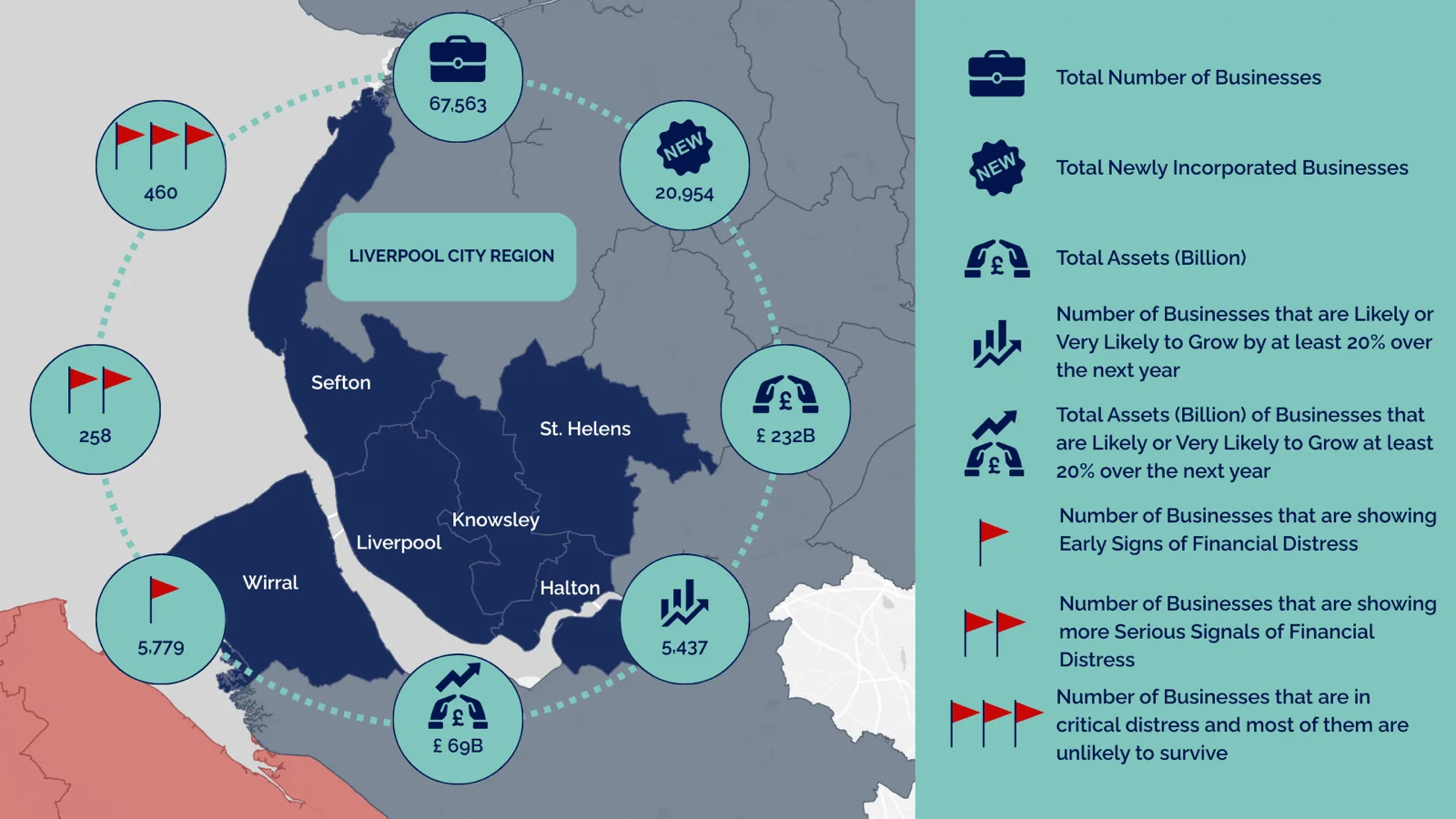

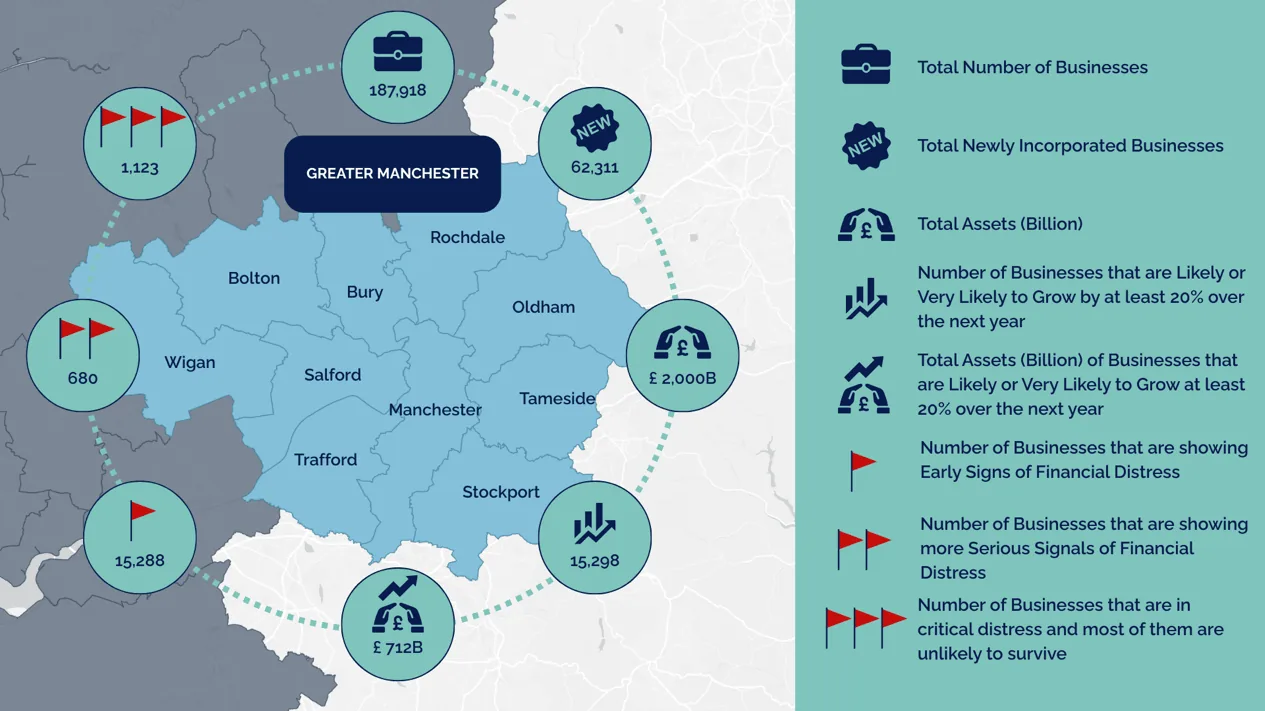

THE LIVERPOOL AND MANCHESTER CITY REGION BUSINESS OVERVIEW

GC Insights also provided more focussed analyses of businesses within the Liverpool and Manchester City Regions (Figures 15.6 and 15.7).

This highlights the power of these two globally recognised Northwest England cities and their importance as key city regions within the Irish Sea Rim, with well over £2,000 billion in combined assets (Note: figure for Manchester includes assets of international banks in the city).

REGIONAL RESEARCH AND DEVELOPMENT INVESTMENT

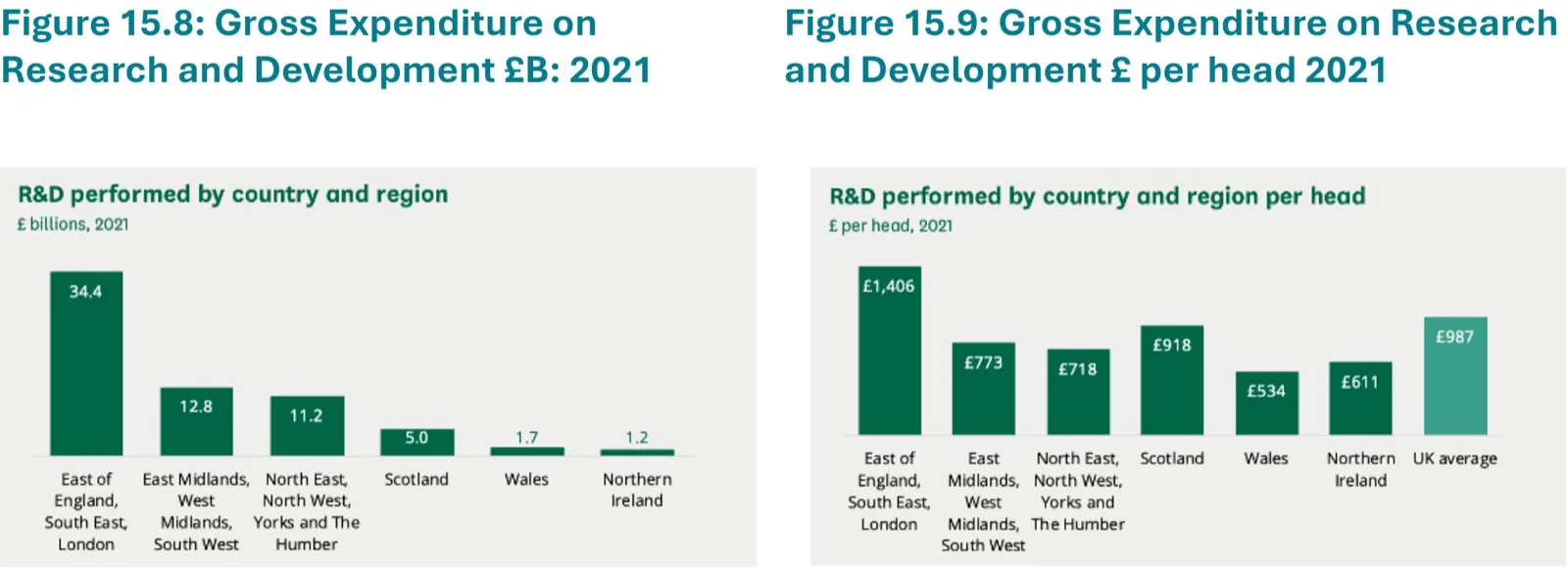

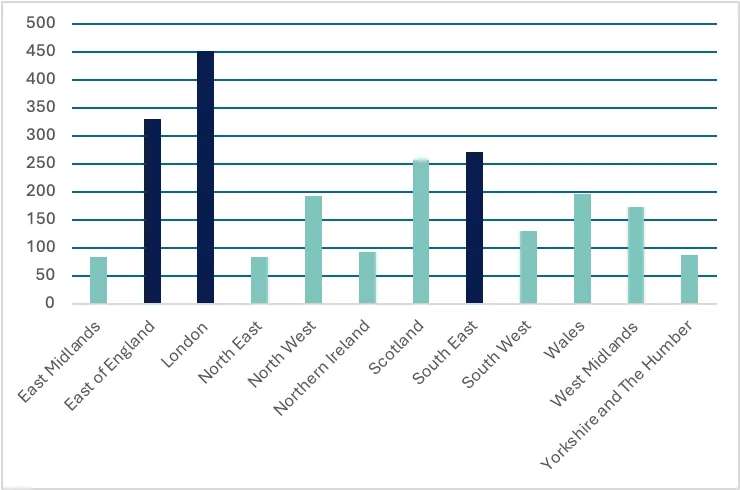

Within the UK, Research and development investment shows a significant imbalance, with research capacity in the UK being disproportionately concentrated around London and South East England. A 2023 House of Commons Library report showed that while the ratio of total 2021 Gross Expenditure on Research and Development (GERD) for the Greater South East compared with the rest of the UK was 1.07 (£34.4 billion vs £31.9 billion) (Figure 15.8), a population-based expenditure per head analysis showed significant regional variation, from £1,406 per person in the Greater South East, to £534 per person in Wales (Figure 15.9)[49]

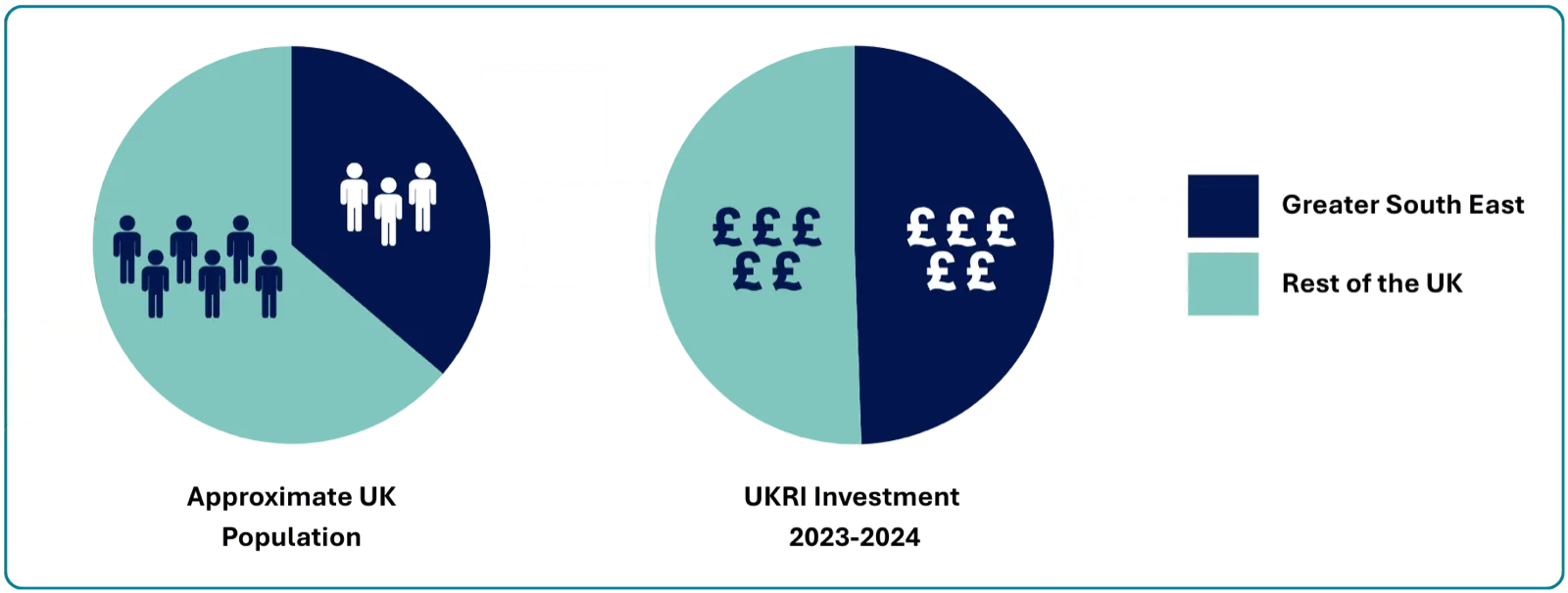

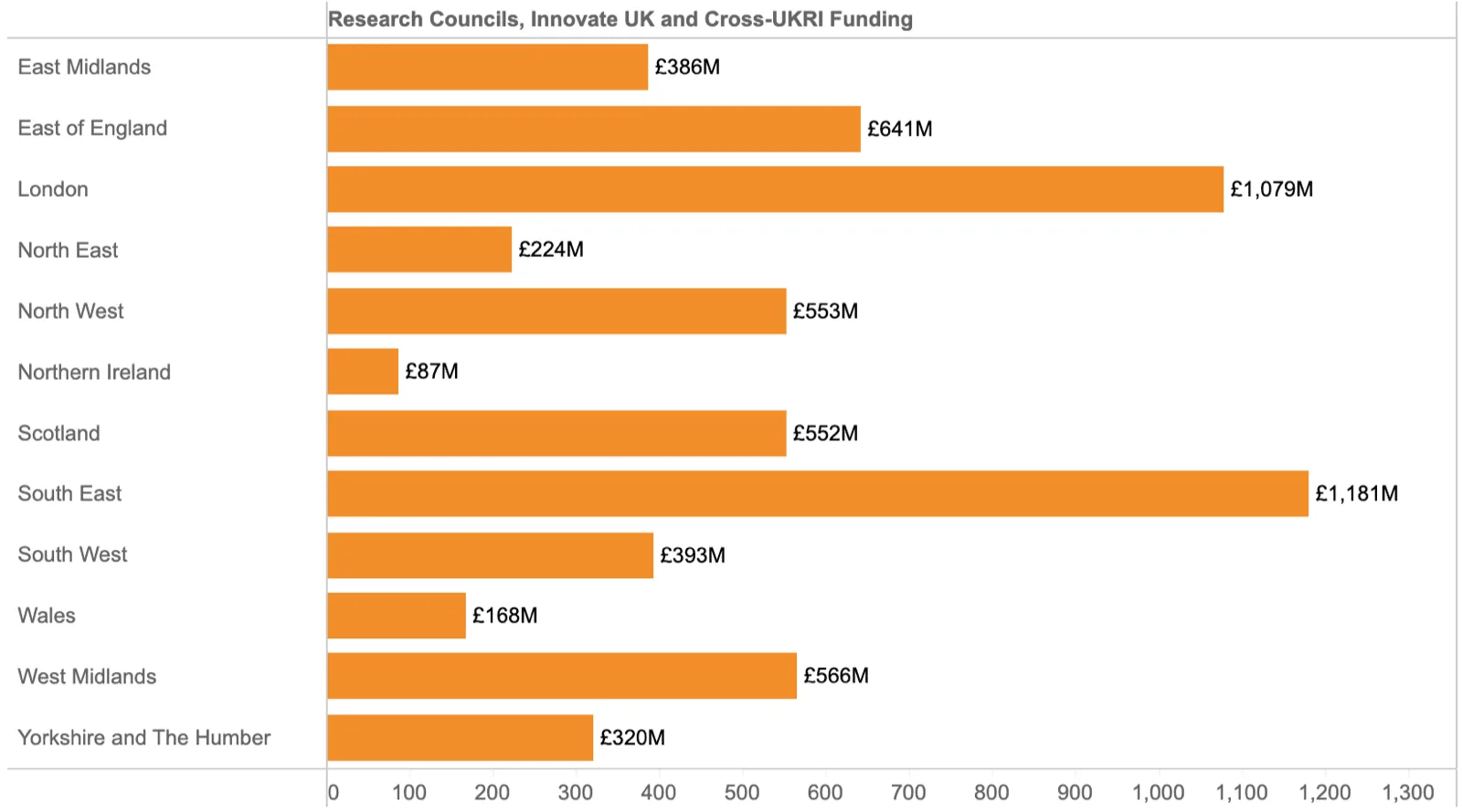

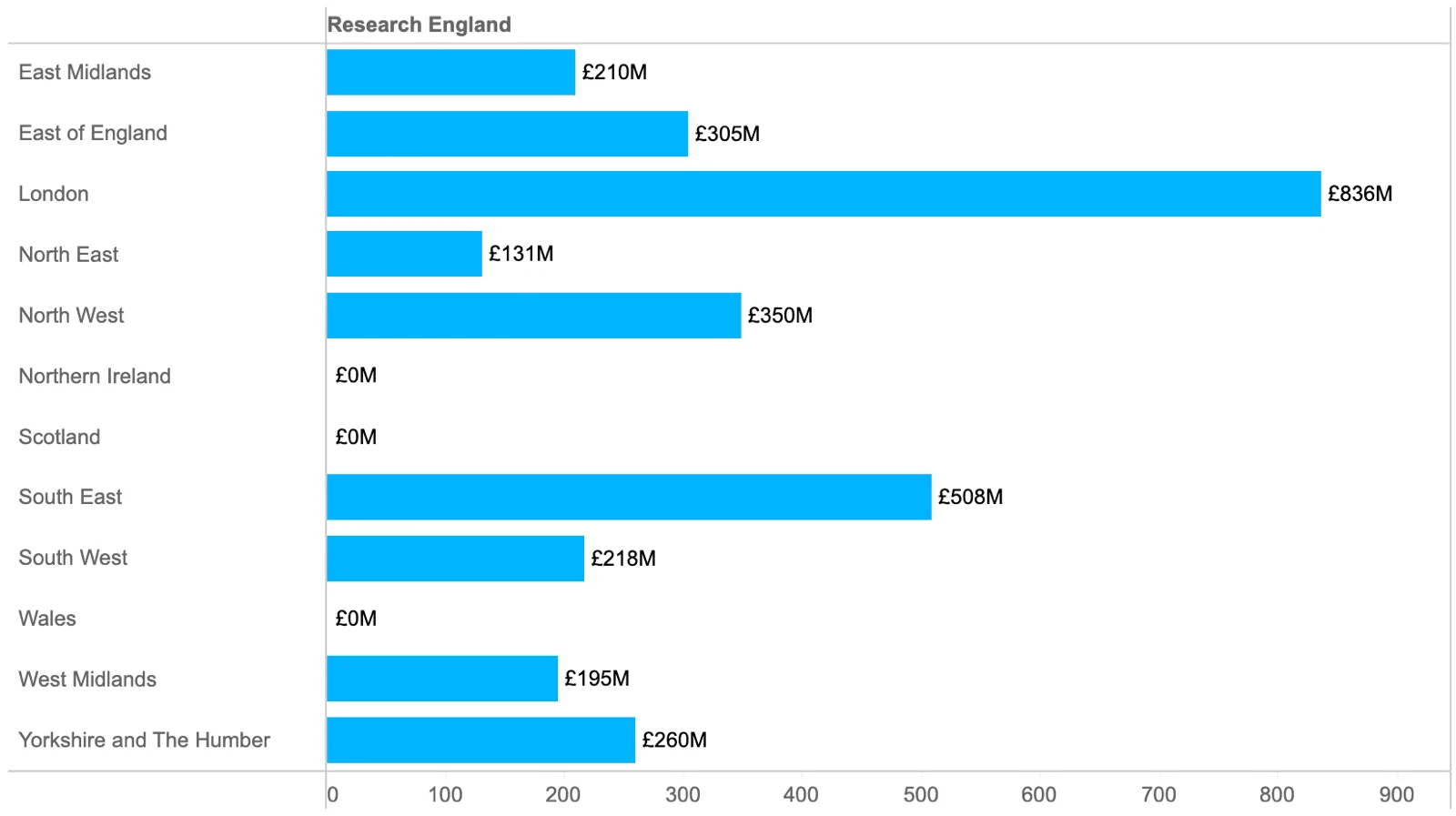

Similarly, UK Research and Innovation (UKRI) investment data show a long-term concentration of investment in the Greater South East. The 2023-2024 financial year was the first in which UKRI invested more in the rest of the country compared with the Greater South East (£4,614 million vs £4,550 million)[50]. However, 50% of UKRI investment is still concentrated within the Greater South East, and significant regional disparities remain for Research Councils, Innovate UK, and Cross-URKI (Figure 15.11) and Research England-specific funding (Figure 15.12).

For reference, the combined population of London, the South East, and East of England is ~25 million compared with ~44 million in the rest of the UK (Figure 15.10).

Source: URKI[51]

Source: URKI

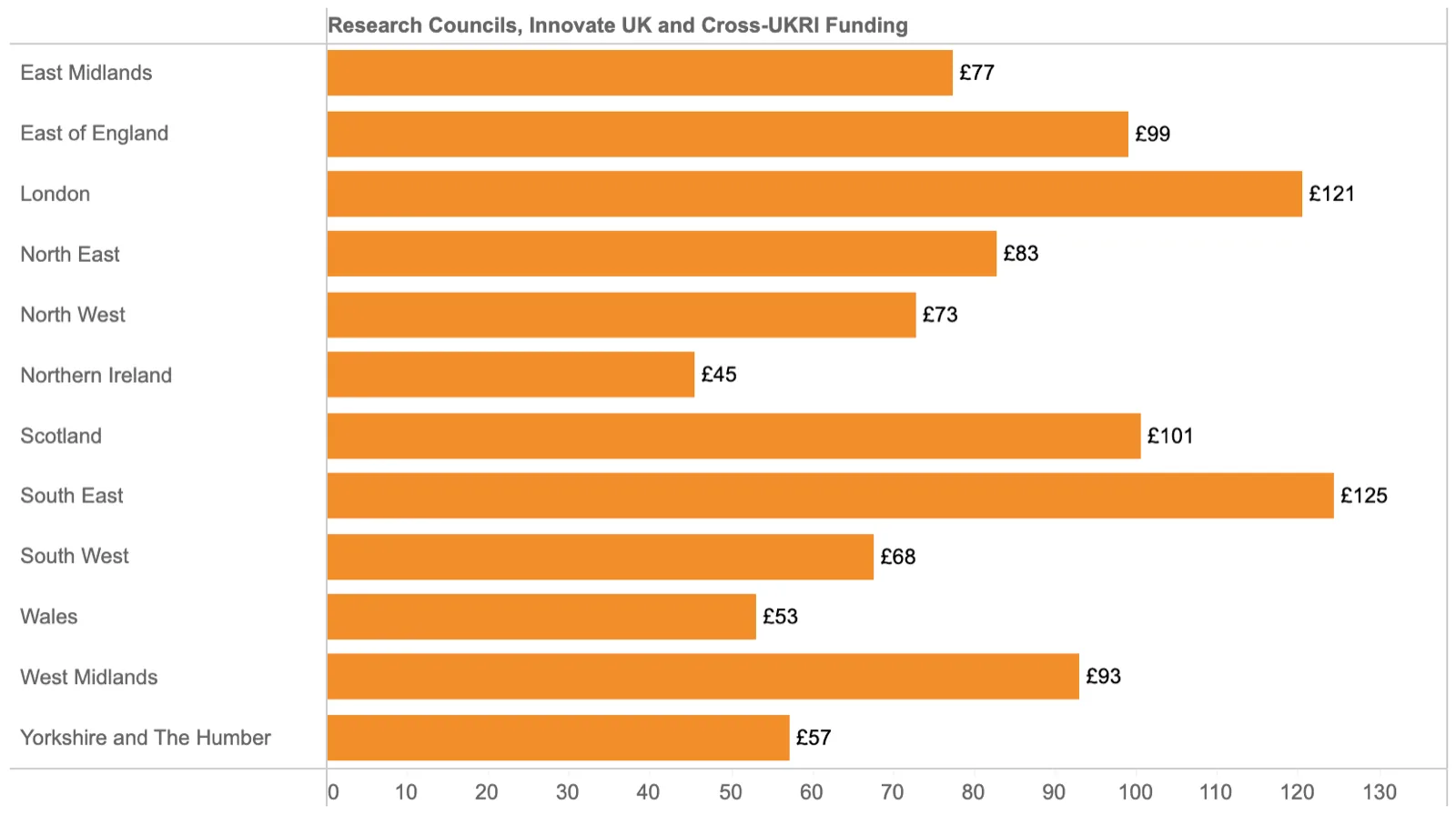

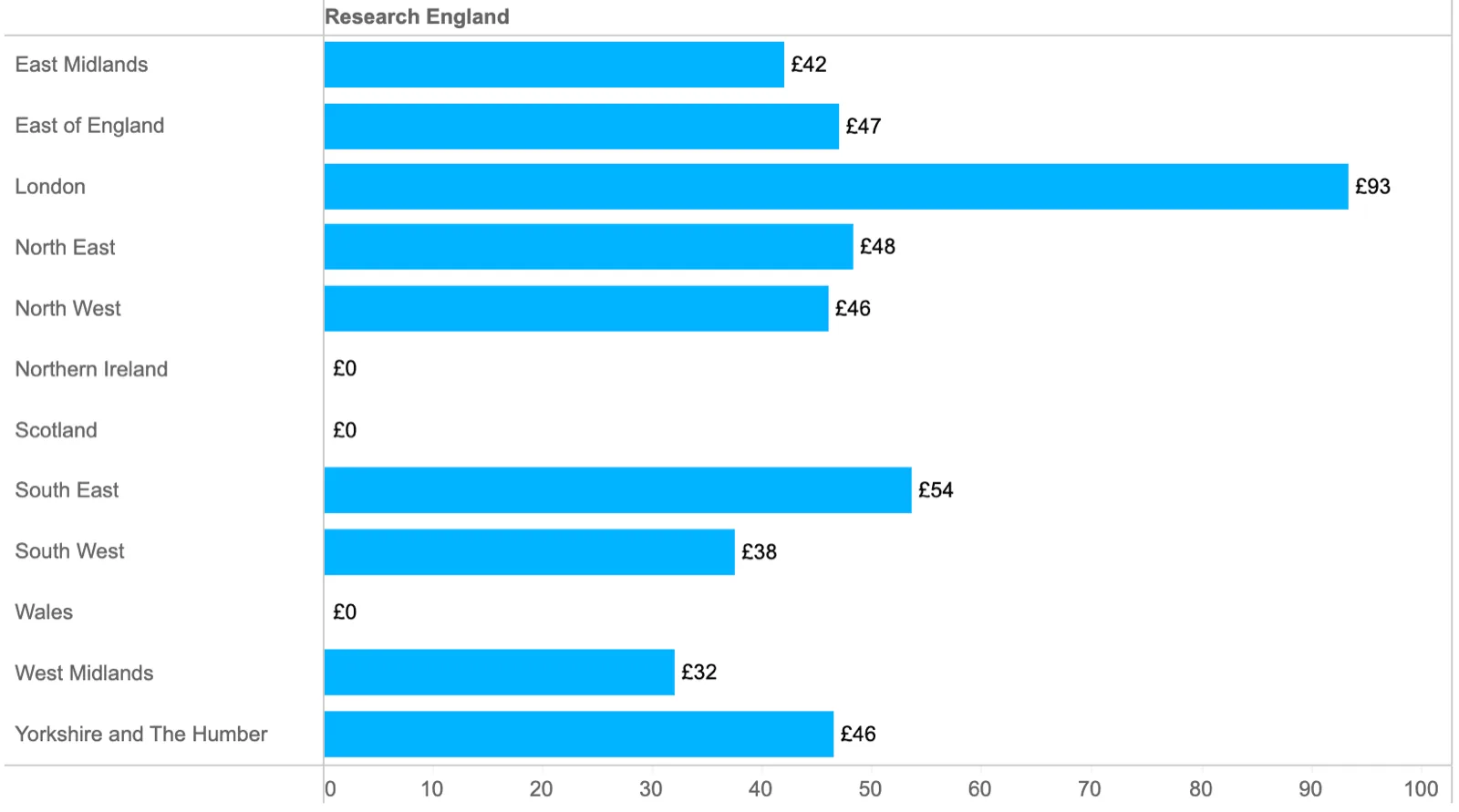

UKRI investment per person has increased in recent years. It is positive that the ratio between the Greater South East and the rest of the UK has fallen from 2:1 to 1.7 in recent years, however, investment per person remains substantially higher in the Greater South East (£183) compared with the rest of the UK (£106). Figures 15.13 and 15.14 show investment per person for UK regions for Research Councils, Innovate UK, and Cross-URKI, and Research England.

Figure 15.13: Geographical Distribution of UK Research Councils, Innovate UK, and Cross UKRI Investment Per Person £ – Financial Year 2023-24

The Irish Sea Rim will work closely with partners in Ireland to evaluate the research and innovation investment landscape and identify priorities for funding and rebalancing.

In a 2024 report on regional research capacity, the Higher Education Policy Institute (HEPI) highlighted that research and development investment and activity is not distributed evenly across each region[52]. There is significant concentration within key cities such as Birmingham, the M62 corridor and the Scottish central belt, with much of the focus on research collaboration being international rather than intra-regional. This leaves wider regional networks across the West Midlands, the North West, Yorkshire and the Humber and across Scotland underdeveloped, leaving many populations and communities in these areas underserved. This is particularly relevant for coastal communities around the Irish Sea Rim.

A July 2025 report by the Committee of Public Accounts (PAC) on UK Research and Innovation[53] emphasised the vital role that UKRI plays in developing and maintaining the UK’s research and innovations system. However, the report also highlighted that there is a lack of a joined up, coherent set of priorities set by the Department of Science, Innovation and Technology (DSIT) which should inform UKRI’s strategic approach.

UK RESEARCH AND INNOVATION STRATEGIC UPDATE

In response UKRI’s updated funding settlement, there has been a marked shift from Research Council-led allocation of research and innovation funding towards a more explicitly strategic, outcome-focused investment model aligned with the UK Government’s Modern Industrial Strategy, wider public missions, and the Plan for Change. Across the 2026/27 – 2029/30 Spending Review period, the Department for Science, Innovation, and Technology (DSIT) has allocated £38.6 billion to UKRI, with UKRI’s annual budget rising from £9.2 billion in 2026/27 to almost £10.0 billion by 2029/30. This sits within DSIT’s wider £58.5 billion R&D budget and the Government’s stated £86 billion public R&D commitment over the Spending Review period. The new approach is intended to protect foundational discovery research while more deliberately using public R&D as a lever for productivity, private investment, industrial capability, technology adoption and national renewal.

From April 2026, the majority of UKRI funding will be allocated through three main priority “buckets”, underpinned by a fourth enabling bucket. The largest bucket is curiosity-driven, foundational research, receiving £14.5 billion over the period, including £3.3 billion for applicant-led research, £8.9 billion for quality-related research funding to English universities, and £2.3 billion for other discovery-enabling investments such as institutes, infrastructures, open access and metascience. The second bucket, strategic government and societal priorities, will receive £8.3 billion, including £6.8 billion of programmatic support for Industrial Strategy sectors and wider government priorities, £500 million for the R&D Missions Accelerator Programme, and £750 million for large-scale national compute. The third bucket, supporting innovative companies, will receive £7.4 billion, including £5.1 billion for Industrial Strategy sectors and wider government priorities, £1.8 billion for knowledge exchange, translation and commercialisation, and £440 million for the Local Innovation Partnership Fund. A fourth enabling bucket of £8.4 billion will support the underpinning capabilities required across the system, including institutes, collective talent, infrastructure, international partnerships and UKRI transformation.

The strategic significance of the settlement is that UKRI is now being positioned more explicitly as a delivery partner for the UK’s 10-year Modern Industrial Strategy. The Industrial Strategy identifies eight growth-driving sectors: Advanced Manufacturing, Clean Energy Industries, Creative Industries, Defence, Digital and Technologies, Financial Services, Life Sciences, and Professional and Business Services. UKRI will establish cross-UKRI programmes across the strategic priorities and innovative companies’ buckets, to create more coherent points of engagement for government, industry, investors, universities and research organisations. Targeted investment across Industrial Strategy sectors totals £9.0 billion within the two mission-facing buckets, with the largest combined allocations going to Digital and Technologies, including AI (£1.584 billion), Quantum Technologies (£1.013 billion), ACT / Semiconductors/Cybersecurity (£718 million), and Engineering Biology (£643 million), alongside Life Sciences (£1.508 billion), Advanced Manufacturing (£1.336 billion), Clean Growth and Energy (£1.176 billion), Defence and National Security (£555 million), Creative Industries (£369 million), and Professional, Business and Financial Services (£118 million). Wider priorities, including climate adaptation, environment and resilience, space, and food, animal and plant health, account for a further £2.944 billion.

For the Irish Sea Rim, the funding architecture creates a clear strategic alignment opportunity, as its key sectors and Economic Engines model map strongly onto UKRI’s emerging priorities: place-based innovation leadership through the Local Innovation Partnership Fund:

- Industrial translation through Innovate UK, Catapults, HEIF and proof-of-concept mechanisms

- Infrastructure and skills through the enabling bucket

- Sectoral alignment through clean energy, advanced manufacturing, maritime and ports, logistics, cybersecurity, creative industries, life sciences and professional services.

The Irish Sea Rim’s Economic Engines model is particularly relevant to the strategic shift towards cross-UKRI programmes, private leverage and outcome-led investment, as this is designed to connect government, industry, academia and place around investable, productivity-enhancing propositions. In practical terms, the Irish Sea Rim not only acts as a powerful regional collaboration platform, but also as a delivery vehicle capable of aggregating demand, aligning innovation assets, de-risking cross-border investment, and translating UKRI and Industrial Strategy priorities into bankable, place-based growth projects across the Irish Sea economy.

THE RESEARCH AND KNOWLEDGE EXCHANGE LANDSCAPE

The 2024 HEPI report also highted the critical importance of research and knowledge exchange in underpinning wider wealth creation and quality of life through ‘the training of highly qualified people, the development of knowledge capacity, and the delivery of innovation’. Yet the report also notes that, despite the concentration of research and development within the Greater South East, this area ‘does not evidently deliver research that is – on average – much more highly rated, nor does it enhance relative GDP beyond that achieved in other regions’. The report’s second finding is that ‘research quality is more evenly distributed across the UK than is funding or volume output’.

HEPI’s conclusion is that the higher levels of funding within the Greater South East are not driven by, nor do they result in, research that is of inherently higher quality than elsewhere in the UK, and that the higher volume of world leading research in this region is related to the higher concentration of funding, rather than an inherent difference in the capability of the research base. Moreover, the report identifies that higher education institutions which receive relatively less funding deliver outcomes that are ‘of a value equal to those better funded’.

HEPI’s conclusion is that the higher levels of funding within the Greater South East are not driven by, nor do they result in, research that is of inherently higher quality than elsewhere in the UK, and that the higher volume of world leading research in this region is related to the higher concentration of funding, rather than an inherent difference in the capability of the research base. Moreover, the report identifies that higher education institutions which receive relatively less funding deliver outcomes that are ‘of a value equal to those better funded’.

Figure 15.15: UK University spin outs (as of 25th July 2025)

A similar pattern can be seen in the knowledge exchange distribution across UK Universities. The University Spin Out Register provides a publicly curated list of all University spin out companies. As of 25th July 2025, the Register shows a total of 1,052 spin outs from universities in the Greater South East compared with 1,300 in the rest of the UK[54] (Figure 14.15).

THE NEED FOR A STRATEGIC APPROACH TO RESEARCH AND INNOVATION INVESTMENT

One key takeaway from these data is that there is an urgent need for a rethink of the policies and strategies which drive government and UKRI decisions around research and innovation investment in the UK. Traditionally, awards and allocations of funding have been based on a retrospective model – with past performance informing future funding. The track record of any university or research institution is an important criterion in decision-making, yet the systemic imbalances in research and innovation investment outlined above, combined with findings of the HEPI report, highlight that past performance is not necessarily an accurate predictor of the potential future capability and impact of an institution. Basing funding on retrospective measures risks ‘hard wiring’ inequities into the funding model, and makes it challenging for universities to increase performance, due to lack of funds.

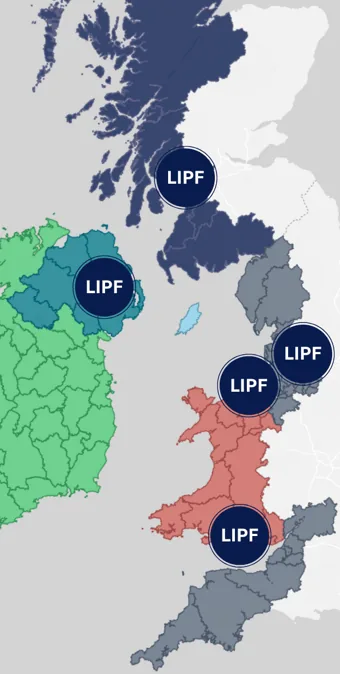

The need for a joined-up strategic approach to regional research and innovation across the whole UK was further highlighted by two UKRI announcements in July 2025. The first launched the Local Innovation Partnership Fund (LIPF), a UKRI-led £500m programme to scale high potential innovation clusters around the UK[55]. Of the 10 earmarked regions which will each receive £30m in funding, nine are situated outside the Greater South East, and funds will be released based on future-focussed strategies and project plans. The Irish Sea Rim will work closely with regions around the Irish Sea receiving earmarked funding (Figure 15.16) to connect, bridge, and amplify innovation projects across the quadruple helix of government, business, academia, and place, to support regenerative economic growth and sustainability.

The second announcement outlined the allocation of the £54m URKI Global Talent Fund, which has been established to support selected institutions to recruit and embed teams of international researchers. In contrast to the LIPF, of the twelve institutions which will receive each £4.5m, five are in the Greater South East (including two in Cambridge). While Queen’s University Belfast was successful, no institutions in the North of England received funding. From the information available, investment decisions have been made based on ‘organisational strengths in successfully receiving and using competitive international funding and recruiting and retaining international researchers.’[56] This approach has led to criticism from the N8 Research Partnership.

The Committee of Public Accounts report on UKRI noted that ‘it can be more attractive for investors, and more effective for government, to invest in geographic regions where there are existing clusters of high-quality research, essential infrastructure, and local skills’. To some extent, this explains the continued imbalances in investment across the UK. Yet it also provides a significant opportunity for growth outside the Greater South East. Strategic government and UKRI investment, support, and capacity building in priority regions outside the Greater South East will help amplify previously underfunded clusters of excellence and draw in new investment from UK and global partners.

There is therefore a strong case to be made for strategic connections across, as well as within regions, and that as a collective, the Irish Sea Rim could provide a powerful counterbalance to London and the Greater South East-centric investment, resulting in a significant uplift in world-class research, innovation, and impact. With our neutral, cross-regional, cross-sector focus, and quadruple helix network model of government, business, academia, and place, the Irish Sea Rim provides a powerful conduit and catalyst for identification of priority funding areas, convening of stakeholders and partners and development of projects which are likely to deliver maximum return on investment, not just in research quality, but also in impact, knowledge exchange, and social benefit.